Every personal finance personality online has a strong opinion about debt payoff strategy. Snowball fans cite behavior science. Avalanche fans cite math. Both sides are partially right — and both miss the part that actually matters for your specific situation, which is running the actual numbers on your actual debts and seeing what the difference really is.

For most people, the difference between snowball and avalanche isn’t dramatic. For some, it’s thousands of dollars. The only way to know which category you’re in is to calculate both.

How Each Method Works

Before DDH, I was doing this manually in spreadsheets. Here’s the faster way:

Debt Snowball (Dave Ramsey’s method): Pay minimums on everything. Put all extra money toward the smallest balance first, regardless of interest rate. When that’s paid off, roll that payment to the next smallest balance. Psychological advantage: fast wins, building momentum.

Debt Avalanche (mathematically optimal): Pay minimums on everything. Put all extra money toward the highest interest rate debt first, regardless of balance size. When that’s paid off, roll that payment to the next highest rate. Mathematical advantage: minimum total interest paid.

| Factor | Snowball | Avalanche |

|---|---|---|

| Interest paid | Higher | Lower |

| Time to debt-free | Usually longer | Usually shorter |

| First payoff date | Faster (smallest balance) | Slower (may be large high-rate debt) |

| Psychological reward | More frequent wins | Delayed reward |

| Best for | Many small debts, motivation challenges | High-rate debt concentration, math-motivated people |

When the Difference Is Dramatic (And When It Isn’t)

The gap between snowball and avalanche is largest when your highest-interest debt is also your largest balance. In that case, you’d spend years paying minimums on the high-rate debt while zeroing out small balances — costing significant interest over time.

The gap is small when your debt structure looks like this: several debts of similar size with clustered interest rates (e.g., three credit cards all between 19-24%). When rates are similar, the method matters less than the consistency of execution.

Example where the gap is significant: $25,000 car loan at 6% (large, low rate) + $8,000 credit card at 26% (smaller, high rate). Snowball says pay the car loan first. Avalanche says pay the credit card first. The avalanche method saves you approximately $4,000-$6,000 in interest in this scenario — and finishes faster. The “psychological wins” argument doesn’t survive a $5,000 counterargument.

How the VVS Debt Payoff Calculator Works

The Vault & Vessel Debt Payoff Dashboard (from our VVS Etsy shop) runs both scenarios on your actual debts simultaneously. You enter each debt: name, balance, interest rate, minimum payment. Enter your total monthly debt payment budget. The dashboard projects both methods side by side: months to debt-free, total interest paid, and the dollar difference between methods.

It also handles the hybrid approach — pay off a small balance first for the psychological win, then switch to avalanche for remaining debts. For many people, this hybrid is the actual best approach: one quick snowball win to prove the system works, then ruthless avalanche discipline for the rest.

🎁 Free Debt Payoff Calculator Template

The Behavioral Science Case for Snowball (And Its Limits)

The academic case for snowball comes primarily from a Harvard Business Review study (Amar et al., 2011) showing that people were more motivated and made larger total payments when focusing on smaller balances. This is real. Motivation matters when the alternative is giving up entirely.

The limits: this research was done in lab conditions with controlled payment scenarios, not with people who have access to a calculator showing them the $5,000 difference in interest. Information changes motivation. When people see the actual dollar cost of the snowball method on their specific debts, many become highly motivated by the avalanche method instead.

The real question is: what motivates YOU? If you’ve tried avalanche before and quit because you couldn’t see progress, snowball’s frequent wins might be worth the interest premium. If you’re math-motivated and the interest calculation makes the avalanche feel urgent — use it.

The Factor Nobody Talks About: Interest Rate Changes

If any of your variable-rate debts (HELOCs, adjustable-rate credit cards, student loans on income-driven plans) may change rates, run the avalanche calculation on the current rates AND on a scenario where those rates increase 2-3%. If the avalanche winner switches with a rate change, that’s important information for your strategy.

Also: if you have any debt with a promotional 0% APR period, that debt’s “real” interest rate is 0% until the promo ends — treat it accordingly. Put it last in the avalanche order until the promo expires, then move it to the front.

For the savings side of debt payoff strategy, our emergency fund guide covers how much cash to keep while aggressively paying debt — getting this wrong is a common reason debt payoff plans derail. And our zero-based budgeting guide shows how to find the extra monthly payment that accelerates either method.

Run the calculation. See the actual dollar difference for your specific debts. Then decide based on data and honest self-knowledge — not a personality quiz or internet forum conviction.

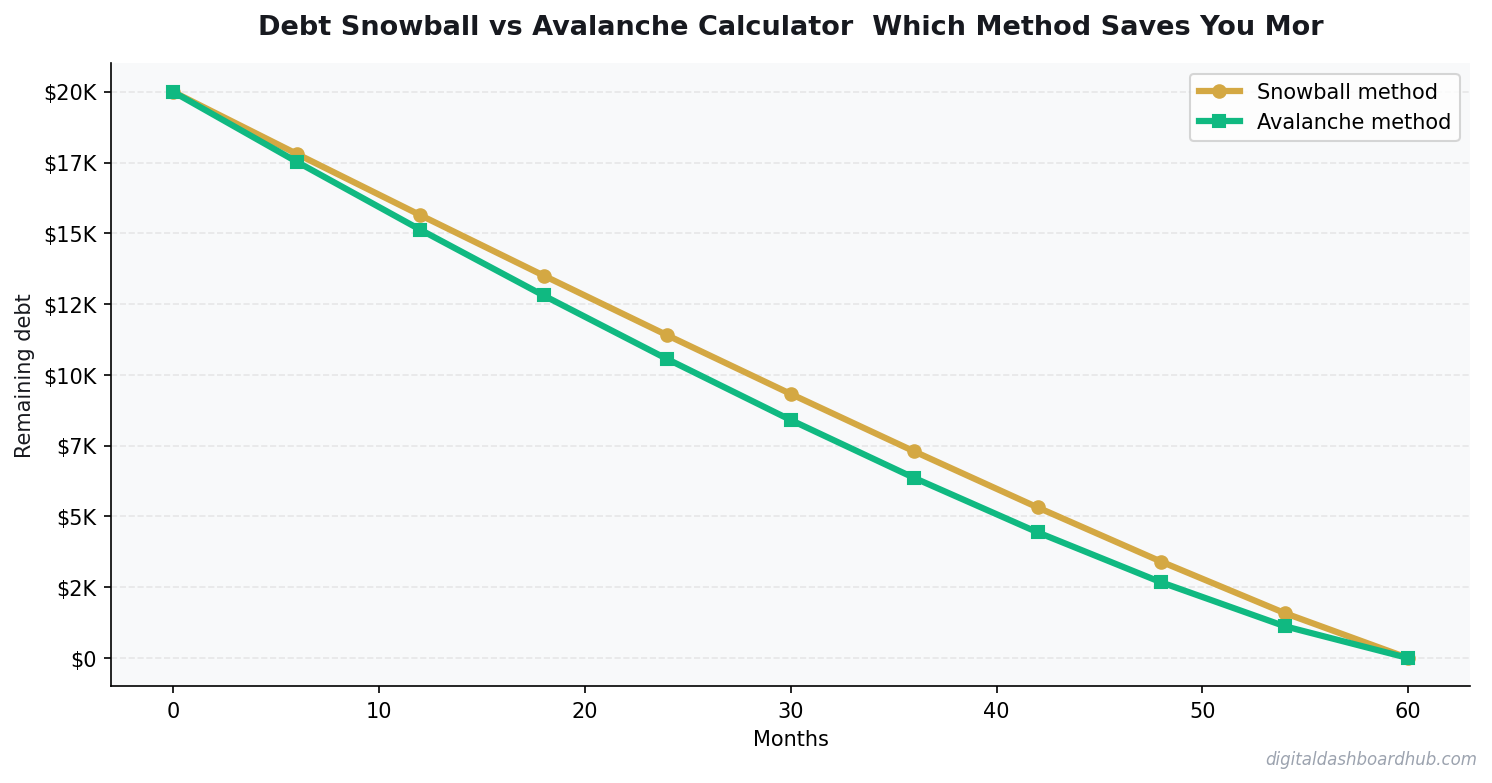

A Worked Example: $23,400 in Debt, Two Strategies Head to Head

Meet someone carrying three debts: a credit card at 24.99% APR with a $4,200 balance, a personal loan at 11% APR with a $9,000 balance, and a car loan at 6.9% APR with a $10,200 balance. They have $600/month to throw at debt after minimums.

Snowball method (smallest balance first): They attack the credit card first, then the personal loan, then the car. Debt-free in about 44 months, paying roughly $5,100 in total interest.

Avalanche method (highest rate first): Same credit card first (it’s also the highest rate here, so same order). They’re debt-free in about 43 months, paying roughly $4,600 in total interest. Saves about $500.

The math difference is real but small. The motivation difference is where the real money is.

The Psychological Case for Snowball That Math Doesn’t Capture

Research on debt payoff behavior consistently finds that people who pay off individual accounts — even sub-optimal ones — are more likely to stay the course. The act of closing a credit card account completely fires a different part of the brain than watching a large balance shrink by 3%. If you’ve tried avalanche and quit, snowball will save you more money. Not because the math is better, but because finishing beats optimizing.

The “best” debt payoff strategy is the one you actually follow for 3-4 years. Don’t let perfection be the enemy of paid off.

The One Mistake That Derails Both Methods

Not freezing the credit card. If you’re aggressively paying down a card while also adding new charges to it, you’re running on a treadmill. The minimum payments go up, the progress feels invisible, and most people quit within 6 months. The brutal but effective move: cut or freeze the card, move to a debit-only system for discretionary spending, and treat the payoff plan as a fixed 3-year project. It’s supposed to feel constraining — that’s the point.

One More Thing: What Happens After You’re Debt-Free

The payoff isn’t the finish line — it’s the launch pad. Whatever monthly payment you were sending to debt (say, $600/month) doesn’t disappear when the debt is gone. That cash flow is now yours to redirect. The people who stay financially healthy after debt payoff treat that freed-up cash intentionally: straight to a 3-6 month emergency fund first, then to retirement accounts, then to investing.

The ones who struggle rebuilt debt within 2-3 years of paying it off — usually because the underlying spending pattern didn’t change, just the debt vehicle. The calculator solves the math problem. The discipline problem is harder and more personal. Know which one you’re actually working on.

Keep reading (related guides):

255+ interactive tools for your money, time, and health.

Full dashboard access · Stripe-secure checkout · Cancel anytime

Disclaimer: This article is for educational purposes only and does not constitute financial advice. Debt situations vary; consult a qualified financial advisor or credit counselor for guidance specific to your circumstances.

Keep Reading

- I Tested 9 Expense Tracker Apps for 3 Months — Here’s What Actually Worked

- Freelancer Finance Management Dashboard (VVS): Finally, a Money Tool Built for Variable Income

- Airbnb Revenue Calculator: Estimate Your Short-Term Rental Income Before You List

Andy Gaber is the founder of Digital Dashboard Hub, a suite of 255+ interactive financial, productivity, and wellness tools. He built DDH after getting frustrated with financial apps that gave outputs without context. Follow along for tool tutorials, revenue analytics breakdowns, and honest takes on personal finance.