You Know Roofing Pays Well — But You Don’t Know Exactly How Well Until You Run the Numbers

Scroll down — the interactive tool runs live with your inputs. Full version lives inside Digital Dashboard Hub. Two-click trial, Stripe-secure.

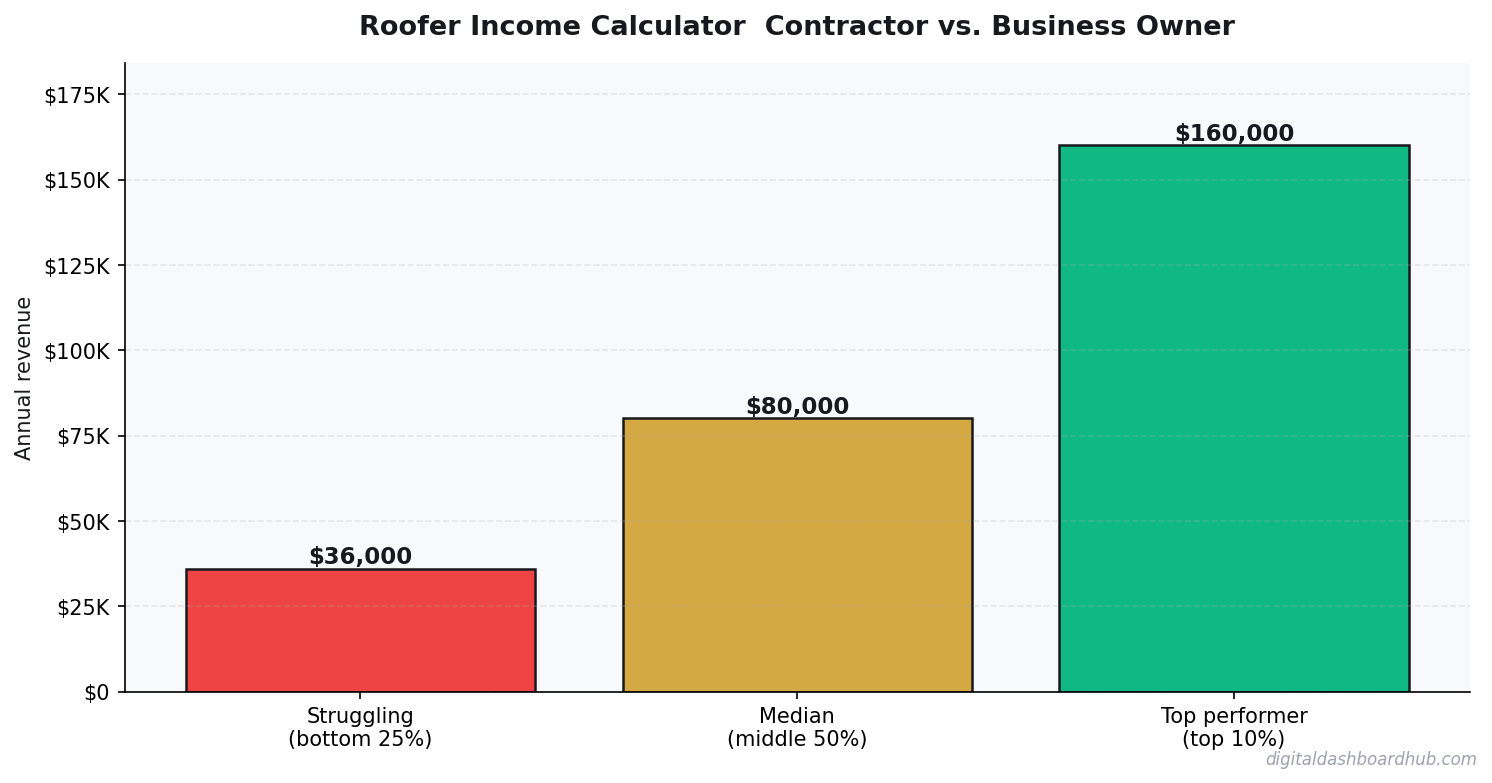

A skilled roofer can make $45K or $300K depending on one decision: whether they stay on someone else’s crew or build their own. The work is the same shingles, the same flashing, the same brutal summer heat. The income difference is entirely about business structure.

I’ve broken down the three paths — employee, subcontractor, and roofing company owner — with real numbers so you can see exactly where you fall and where you could be.

Three Paths, Massive Income Spread

The jump from employee to subcontractor is significant. The jump from subcontractor to owner is where generational wealth gets built — or where people go broke. Let’s dig into each.

Employee Roofer: Steady but Capped

An entry-level roofer makes $15–$20/hour ($31K–$42K). With 3–5 years of experience, that climbs to $22–$30/hour ($46K–$62K). Foremen and lead roofers top out at $28–$35/hour ($58K–$73K) in most markets.

The upside: predictable paycheck, workers’ comp coverage, no business overhead. The downside: your ceiling is your hourly rate × available hours. You’re trading body for dollars with no equity being built.

Regional variation matters enormously. The same experienced roofer earns:

- Southeast (FL, GA, AL): $18–$26/hr

- Midwest (OH, MI, IN): $22–$30/hr

- Northeast (NY, MA, CT): $28–$40/hr

- West Coast (CA, WA): $30–$45/hr

Subcontractor: Better Money, More Responsibility

As a subcontractor, you bid on jobs from general contractors or roofing companies. A typical residential re-roof pays the sub crew $3,000–$6,000 for labor. If you’re running a 3-person crew, your costs are $1,200–$2,000 in labor to your helpers, plus $300–$500 in equipment wear and fuel. Your take: $1,300–$3,500 per job.

At 3–4 jobs per week during peak season (April–October) and 1–2 per week in the off-season, annual revenue lands around $150K–$250K. After crew pay, truck costs, insurance ($3,000–$6,000/year), and tools, your net: $55,000–$110,000.

The catch: no work means no income. Rain weeks, slow winters, and gaps between jobs can eat 20–30% of your potential earning days. Most subs actually work 180–220 days per year, not 260.

How does your specific market compare? The roofer income calculator lets you input your local job rates, crew size, and seasonal patterns to get a real projection.

Roofing Company Owner: Where the Real Money Lives

A roofing company owner doesn’t just do roofs — they sell roofs. The average residential re-roof costs the homeowner $8,000–$15,000. Materials run $3,000–$5,500. Labor (your sub crews): $2,500–$4,500. Your gross profit per job: $2,000–$5,000.

A company doing 200 roofs/year (about 4/week) at $3,500 average gross profit = $700,000 in gross profit. After office overhead ($60K), insurance ($15K–$25K), truck payments ($24K–$36K), marketing ($30K–$60K), and admin staff ($40K–$50K), owner’s take: $150,000–$300,000+.

The Scale Math

This is what makes roofing company ownership so lucrative: you can run multiple crews. Each crew you add is another $200K–$500K in revenue with roughly the same office overhead. A 3-crew operation doing 500+ roofs/year can generate $500K+ in owner profit.

Storm chasers — companies that follow hail and wind damage — can do even better. A single major hailstorm can mean 50–100 insurance jobs at $12K–$20K each in a matter of weeks.

The Costs of Going Independent

Before you see dollar signs, what my data showed you need to start a roofing company:

- Contractor’s license and bond: $2,000–$10,000 (varies wildly by state)

- General liability insurance: $5,000–$15,000/year

- Workers’ comp insurance: 15–30% of payroll (this is the big one)

- Truck and trailer: $25,000–$50,000

- Tools and equipment: $5,000–$10,000

- Marketing and first-job costs: $5,000–$15,000

Total startup: $50K–$100K minimum. Many owners bootstrap by subcontracting for 2–3 years, saving aggressively, then launching their own company with cash reserves and a referral network.

I built a roofing business startup cost worksheet and break-even calculator that maps your path from sub to owner. Grab it free when you start your trial.

Seasonal Cash Flow: The Hidden Challenge

Roofing revenue isn’t flat. A typical pattern:

- January–February: 30–50% of peak revenue (weather delays, fewer leads)

- March–May: Ramp-up to 80–100% (spring storm season, homeowner projects)

- June–September: 100% peak (longest days, most jobs)

- October–November: 70–90% (pre-winter rush)

- December: 40–60% (holiday slowdown)

Smart owners save 20–25% of peak-season profits to cover winter payroll and overhead. The ones who don’t end up laying off crews every December and scrambling to rehire every March.

What to Do Now

- Know your number. Open the roofer income calculator and input your current path — employee, sub, or owner. See the 5-year trajectory for each option with your local rates.

- Get your contractor’s license. If you’re a sub without a license, this is the single highest-ROI move. It opens insurance work, commercial jobs, and direct-to-homeowner sales.

- Build a 6-month cash reserve. Whether you’re going from employee to sub, or sub to owner, having runway makes the transition survivable instead of terrifying.

Over 2,000 contractors and business owners use our financial calculators to make better decisions. Start your free trial and see what your roofing career is really worth.

Roofing Contractor vs. Business Owner: The Real Income Gap

This is a distinction most people in the trades underestimate. A skilled roofer working for a company in Dallas earns $55,000–$75,000/year as a journeyman or foreman. The owner of a 4-crew roofing company in the same market earns $180,000–$350,000/year — or loses everything if they don’t understand their numbers. The gap between employee income and owner income is enormous, but so is the risk differential.

The contractor in between — licensed, owner-operator, solo or with 1 helper — earns $90,000–$140,000 in most markets if they’re organized. Here’s the math: 2 jobs/week at $8,500 average contract value = $17,000/week. After materials (35%), helper ($800), and insurance/fuel ($600): $9,650/week net, or $38,600/month. That’s $463,000/year gross, $250,000–$280,000 net before taxes. This is the math that makes self-employment in roofing compelling.

The Three Things That Separate $100K Roofers from $250K Roofers

Estimating accuracy. A roofer who consistently underbids by 8% is working 8% of their time for free. Good estimators use software (JobNimbus, RoofSnap) and have a realistic labor rate that includes overhead — not just what they pay crews. Most roofing losses come from underestimating labor on complex jobs, not from material pricing.

Commercial vs. residential mix. Residential jobs have lower average contract values but shorter sales cycles. Commercial jobs ($15,000–$200,000) require insurance documentation, bid processes, and longer waits — but they’re less weather-dependent, the relationships are stickier, and the margins are often better. Roofers who develop even 2–3 commercial accounts have a fundamentally more stable business.

Storm work and insurance claims. In hail-prone markets (Texas, Colorado, Oklahoma), roofers who understand the insurance claim process and can help homeowners navigate it command premium pricing and have almost unlimited demand after significant weather events. This is a specialized skill worth developing.

Insurance is the single largest risk variable in the roofing business, and it’s one most new contractors underestimate. A general liability policy for a solo roofer runs $3,000–$6,000/year. Add workers’ comp if you have employees (typically 30–40% of payroll for roofers, one of the highest-risk trades). The contractors who cut corners on coverage are one job site accident away from losing everything they built. Full coverage isn’t optional — it’s the cost of operating a legitimate roofing business.

Keep reading (related guides):

How to Hit Six Figures as a Solo Roofer

The math is straightforward, but most solo roofers never work it backwards. Here is the path from current revenue to a clean $150K owner income.

Start with target income, work backward

If you want $150K take-home, you need $185K-$210K gross after self-employment tax, insurance, and operating expenses. At an average ticket of $10K and 25% net margin, that’s 75-85 jobs per year — about 6-7 completed jobs per month.

Master insurance restoration work

Insurance claims typically pay 15-25% higher per square than retail residential. They also come with built-in marketing — after a hailstorm, your market floods with motivated buyers. Getting HAAG or other adjuster-approved certifications pays for itself in the first three claims.

Don’t compete on price for retail roofs

The bottom 30% of roofers compete on price and barely break even. The top 30% compete on speed, quality, and warranty — and charge 15-30% more. Position your quotes around workmanship warranty, cleanup, and project timeline, not just materials.

Manage crew cost aggressively

Labor is the biggest variable cost for roofers. Solo owners running one crew can see labor swing from 35% to 55% of revenue depending on crew efficiency, weather, and material handling. Track labor cost per square religiously — that one number tells you if you’re actually profitable.

Build for year three, not year one

Year one is chaos. Year two is learning. Year three is when established roofers hit their ceiling. Don’t judge the model by your first twelve months — judge it by whether you’re trending toward 6+ jobs per month at sustainable margin by month 18.

Quick FAQ: Roofer Income

How much does a new roofer earn?

Entry-level laborers earn $18-$26/hour ($38K-$55K annually). Journeyman roofers with 3-5 years experience earn $28-$42/hour ($58K-$88K). Foremen $45-$65/hour plus truck allowance. Owner-operators clear $90K-$200K depending on volume.

What’s the difference between residential and commercial roofing income?

Commercial roofing pays 20-40% more hourly because of higher skill requirements (membrane systems, safety protocols, union labor in some markets). Residential is easier to enter but has more price competition. Most six-figure roofers work both.

How seasonal is roofer income?

Very seasonal in cold climates — 40-50% of annual revenue happens between May and October. Southern markets are year-round but slower in summer due to heat. Smart operators use winter for insurance work (hail, wind damage claims) to smooth the seasonal curve.

What role do insurance claims play?

Huge. In hail or storm-prone markets, 60-80% of a roofer’s annual revenue can be insurance-funded restoration work. Getting certified with major carriers (and understanding the adjuster process) is often the single biggest income lever for a residential roofer.

When should I buy my own trucks vs subcontract?

Once you’re running 2+ full crews consistently. A dedicated truck, dump trailer, and tool inventory run $55K-$80K to build out. If you can’t keep that equipment billing at 70%+ utilization, subcontract or lease instead of buying.

Hiring and Scaling a Roofing Business

Once you’re running one crew consistently, scaling to two crews is where most roofers struggle. Here is the sequence that works, broken into the six moves that separate a solo operator from a real roofing business.

1. First foreman, not first laborer

Hire a foreman before you hire more laborers. A foreman who can run a crew without you unlocks your time for sales and estimating. Without a foreman, you’re just adding labor cost — not capacity.

2. Standardize the estimate process

Build a template estimate, job costing workflow, and materials calculator. This lets anyone in your company quote consistently, not just you. Companies that scale past $500K almost always have a repeatable estimate process — the ones stuck at $300K don’t.

3. Cash flow management first, revenue growth second

Roofing cash flow is brutal. Materials due in 30 days, customer payment in 45-90. Build a minimum $60K working capital reserve before you add a second crew, or the growth will crush you.

4. Safety and insurance compliance

OSHA violations, uninsured workers, and sloppy paperwork kill more roofing businesses than bad marketing. Get OSHA-10 certified. Run workers’ comp audits quarterly. Don’t cut corners — the penalties compound faster than the savings.

5. Truck and equipment financing discipline

Every new truck is $55K-$80K loaded. Finance conservatively — you want payments at 6-9% of crew revenue, not 15%. Overextended equipment debt is the #3 cause of roofing business failure.

6. Sales pipeline separate from delivery

The owner has to be selling at all times. Dedicating a specific number of hours per week to outbound sales, CRM hygiene, and estimate follow-up is the difference between a business that stalls and one that grows.

255+ interactive tools for your money, time, and health.

14 days free · No charge today · 2-click cancel

Keep Reading

- The Side Hustle Tax Trap: Track Every Dollar

- How Sinking Funds Saved Me From Financial Emergencies

- Freelancer Tax Guide 2026

Common Questions About Roofer Income Calculator: Contractor vs. Business Owner

How long does it take to see results?

Most people see meaningful progress within 30-90 days when they apply these strategies consistently. The key is tracking your numbers from day one so you have a baseline to measure against.

What’s the biggest mistake people make?

Trying to do everything at once. Pick one or two strategies from this guide, implement them fully, then layer in additional tactics. Spreading yourself thin is the fastest way to see no results from any of it.

Do I need special tools or software?

Not necessarily to start — but the right tools eliminate hours of manual work. Our free calculators and trackers at Digital Dashboard Hub are a good starting point before you invest in paid software.

Andy Gaber is the founder of Digital Dashboard Hub, a suite of 255+ interactive financial, productivity, and wellness tools. He built DDH after getting frustrated with financial apps that gave outputs without context. Follow along for tool tutorials, revenue analytics breakdowns, and honest takes on personal finance.