That $120K Contract Offer Isn’t What You Think It Is

Before you scroll: the calculator below is running in your browser right now. For the full feature set — saved scenarios, history, exports — open the dashboard.

Someone just offered you $120,000 as a 1099 contractor. Your W-2 job pays $95,000. The contract gig looks like a $25K raise. It’s not — and the gap might go the other direction once you factor in self-employment tax, benefits you’ll buy yourself, and deductions you’ll miss. I made this mistake in 2019 and effectively gave myself a $7,000 pay cut while thinking I got a raise.

The Hidden Costs of 1099 Income

As a W-2 employee, your employer pays half your Social Security and Medicare taxes (7.65%). As a contractor, you pay both halves — that’s 15.3% on your first $168,600 of net self-employment income (2025 rate). On $120K, that’s an immediate $18,360 you don’t see coming if you’ve only ever been an employee.

Yes, you can deduct half of that self-employment tax from your adjusted gross income. But the deduction reduces your income tax, not the SE tax itself. The net cost is still significant.

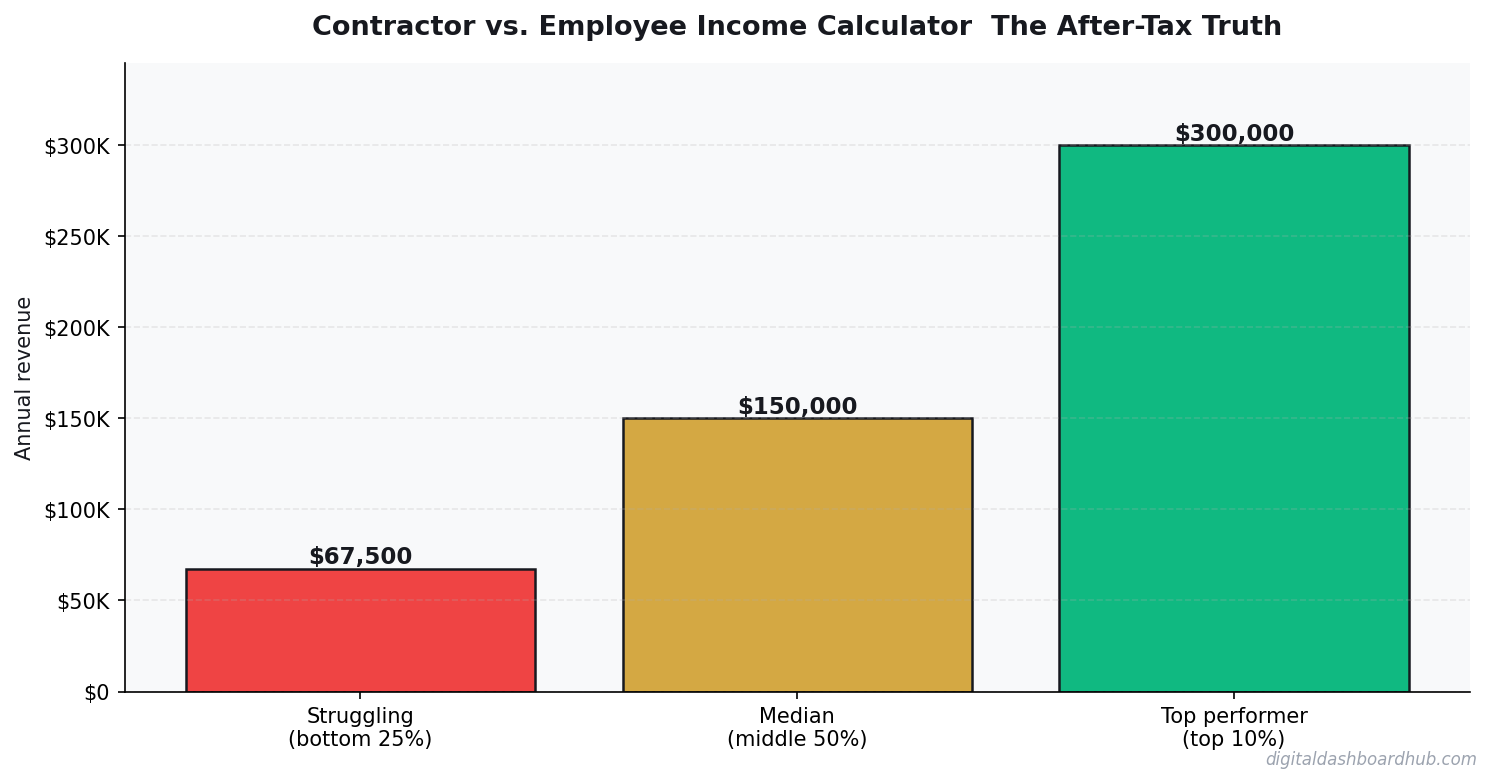

The Full Comparison: $120K Contractor vs. $95K Employee

The $120K contract pays less than the $95K salary in this scenario. Not by a lot, but the person who took the contract thinking they got a 26% raise actually took a 4.4% pay cut.

When Contracting Actually Wins

The math flips when the contract rate is high enough and you take advantage of deductions. Here’s where 1099 income genuinely beats W-2:

- The rate premium is 30%+ over salary equivalent. A $130K+ contract vs. a $95K salary starts to genuinely win after all costs.

- You have legitimate business deductions. Home office ($1,500 simplified or actual), equipment, software, mileage (67 cents/mile in 2025), professional development, internet (business %). These can shave $5,000-$15,000 off taxable income.

- You can open a Solo 401(k). Contribute up to $23,500 as employee + 20% of net SE income as employer contribution. On $120K net, that’s potentially $47,500 in tax-deferred savings — far more than most employer plans allow.

- You qualify for the QBI deduction. The 20% Qualified Business Income deduction can reduce your effective tax rate significantly if your income is under $191,950 (single) or $383,900 (married filing jointly).

Get the Full Comparison Worksheet

I created a detailed side-by-side worksheet that includes all 14 cost categories most people miss (disability insurance, accounting fees, quarterly tax payment opportunity cost, etc.). It’s available when you start a free trial — no credit card, cancel anytime.

The Break-Even Rate

A quick formula to find what 1099 rate equals your current W-2 salary:

Equivalent Contract Rate = W-2 Salary × 1.35 to 1.45

The multiplier accounts for self-employment tax, benefits, PTO, and overhead. For a $95K salary, you need roughly $128K-$138K in contract income to break even. Below that, you’re taking a pay cut with more hassle.

The Non-Financial Factors

Money isn’t the only variable. Some things that don’t show up in a calculator but matter enormously:

- Schedule flexibility — worth $5K-$15K/year to most people if you’re honest about it

- No commute — saves $3,000-$8,000/year in gas, wear, and time

- No office politics — priceless or irrelevant depending on your personality

- Income instability — contracts end, and the gap between gigs can eat your savings fast

- Administrative burden — quarterly taxes, bookkeeping, invoicing, chasing payments. This is real work.

Try This Today

- Calculate your real W-2 total compensation. Base salary + employer FICA + health insurance (employer portion) + retirement match + PTO value. Most people underestimate this by $15K-$25K.

- Multiply that total by 1.15-1.25 to get the 1099 rate where contracting starts to make financial sense (the premium above break-even).

- Run your exact numbers through a dedicated calculator to catch the deductions and costs specific to your situation — state tax rates, filing status, and available deductions change the math significantly.

Our contractor vs. employee calculator factors in all 14 cost categories, state-specific tax rates, and available deductions. Over 500 business owners and freelancers use Digital Dashboard Hub to make smarter income decisions. Start your free trial and see your real numbers in 3 minutes.

The After-Tax Math: Side by Side

Same gross income, radically different take-home. Let’s run a $95,000 equivalent compensation comparison:

Employee at $95,000 salary (single filer, no 401k):

- Federal income tax: ~$16,200

- FICA (employee side 7.65%): $7,268

- State income tax (avg ~5%): $4,750

- Take-home: ~$66,782/year (~$5,565/mo)

Contractor at $95,000 gross (self-employed):

- Self-employment tax (15.3%): $13,560 — but half is deductible

- Federal income tax after SE deduction: ~$14,100

- State income tax (~5%): $4,750

- Business expenses deducted (home office, equipment, health insurance, retirement): -$18,000

- Take-home after taxes, before retirement contributions: ~$56,400/year (~$4,700/mo)

But wait: that contractor also controls their retirement contributions. Max SEP-IRA at 25% of net self-employment income = up to $23,750 pre-tax shelter. After maxing that, their effective tax rate drops significantly. A well-structured contractor can end up with more investable wealth than a $95K employee despite lower take-home pay.

What Most People Get Wrong About This Comparison

They forget the benefits gap. A $95K employee might also have $18,000/year in employer-provided benefits: health insurance, 401k match, paid leave, disability insurance. That raises their true compensation to $113,000. A contractor pricing at $95K gross while ignoring this benefits gap is effectively undercutting themselves by $15,000-$20,000 annually.

The rule: a contractor should charge 1.4-1.6x their equivalent employee salary to come out equal after taxes, benefits, and business expenses. A $95K job requires $133,000-$152,000 in contractor income to truly break even.

The After-Tax Math: Side by Side

Same gross income, radically different take-home. Let’s run a $95,000 equivalent compensation comparison:

Employee at $95,000 salary (single filer, no 401k):

- Federal income tax: ~$16,200

- FICA (employee side 7.65%): $7,268

- State income tax (avg ~5%): $4,750

- Take-home: ~$66,782/year (~$5,565/mo)

Contractor at $95,000 gross (self-employed):

- Self-employment tax (15.3%): $13,560 — but half is deductible

- Federal income tax after SE deduction: ~$14,100

- State income tax (~5%): $4,750

- Business expenses deducted (home office, equipment, health insurance, retirement): -$18,000

- Take-home after taxes, before retirement contributions: ~$56,400/year (~$4,700/mo)

But wait: that contractor also controls their retirement contributions. Max SEP-IRA at 25% of net self-employment income = up to $23,750 pre-tax shelter. After maxing that, their effective tax rate drops significantly. A well-structured contractor can end up with more investable wealth than a $95K employee despite lower take-home pay.

What Most People Get Wrong About This Comparison

They forget the benefits gap. A $95K employee might also have $18,000/year in employer-provided benefits: health insurance, 401k match, paid leave, disability insurance. That raises their true compensation to $113,000. A contractor pricing at $95K gross while ignoring this benefits gap is effectively undercutting themselves by $15,000-$20,000 annually.

The rule: a contractor should charge 1.4-1.6x their equivalent employee salary to come out equal after taxes, benefits, and business expenses. A $95K job requires $133,000-$152,000 in contractor income to truly break even.

Keep reading (related guides):

- Mortgage Comparison Calculator: Find the Best Rate and Term

- How to Calculate Your Freelance Rate (So You Stop Undercharging)

- Profit Loss Statements Arent Scary: A Plain-English Guide for Solo Business Owners

- Freelancer Finance Dashboard: Track Income, Taxes, and Cash Flow in One Visual Hub

- Amazon FBA Revenue Calculator: What Sellers Actually Make in 2026

255+ interactive tools for your money, time, and health.

14-day trial · Stripe checkout · Cancel anytime

Keep Reading

- Freelancer Tax Guide 2026: What to Track All Year

- The Side Hustle Tax Trap: Track Every Dollar

- Freelancer Finance Dashboard

Common Questions About Contractor vs. Employee Income Calculator: The After-Tax Truth

How long does it take to see results?

Most people see meaningful progress within 30-90 days when they apply these strategies consistently. The key is tracking your numbers from day one so you have a baseline to measure against.

What’s the biggest mistake people make?

Trying to do everything at once. Pick one or two strategies from this guide, implement them fully, then layer in additional tactics. Spreading yourself thin is the fastest way to see no results from any of it.

Do I need special tools or software?

Not necessarily to start — but the right tools eliminate hours of manual work. Our free calculators and trackers at Digital Dashboard Hub are a good starting point before you invest in paid software.

Andy Gaber is the founder of Digital Dashboard Hub, a suite of 255+ interactive financial, productivity, and wellness tools. He built DDH after getting frustrated with financial apps that gave outputs without context. Follow along for tool tutorials, revenue analytics breakdowns, and honest takes on personal finance.