I spent last Tuesday night plugging real chiropractic numbers into every calculator I could find. Most of them were garbage — pre-filled with unrealistic inputs and no way to adjust overhead. So I built one that actually works.

Use the Free Chiropractic Tool

The dashboard below loads instantly in your browser. Plug in your numbers, see your answer. No signup to try the basics.

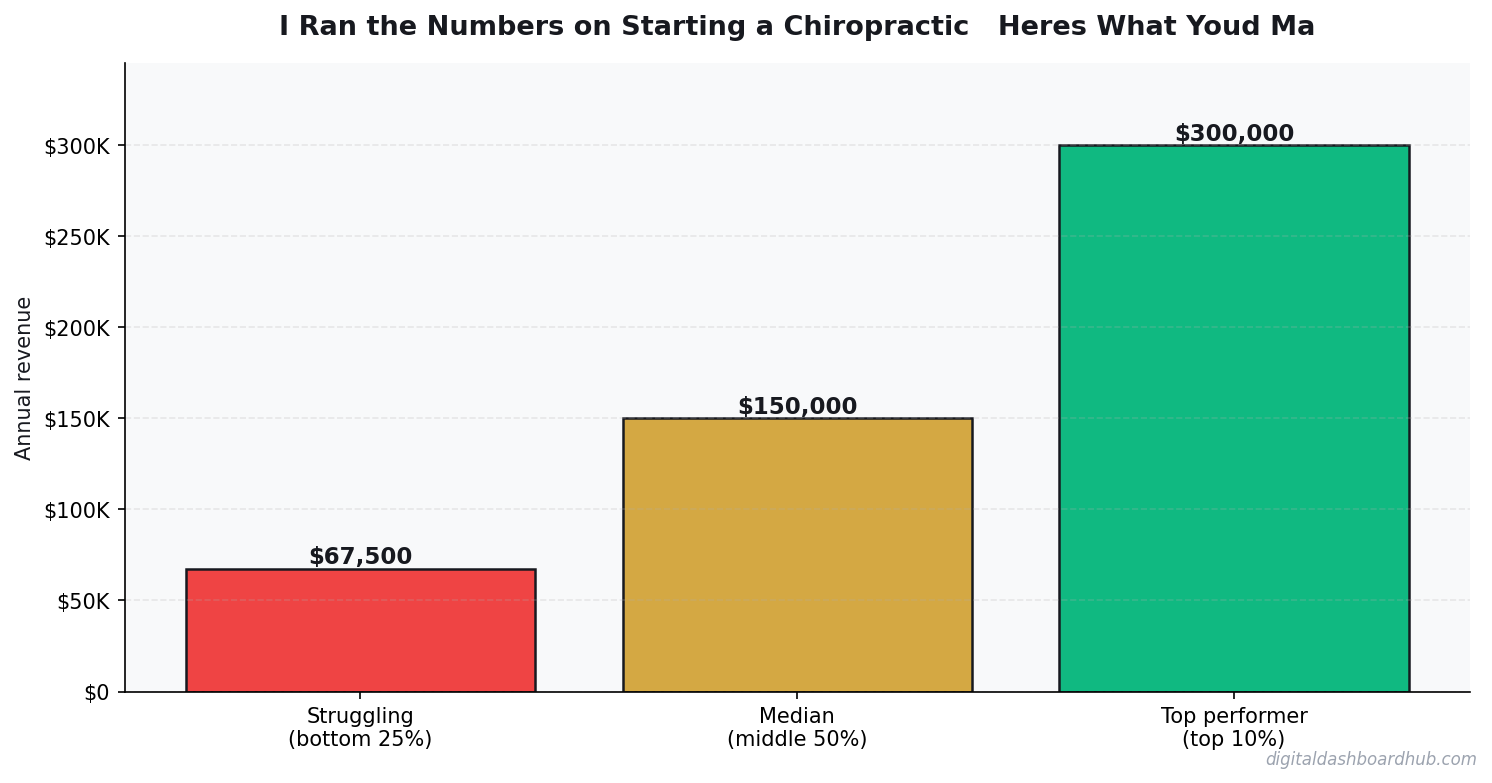

What Chiropractic Practice Owners Actually Take Home

A solo chiropractor seeing 80-120 patients/week grosses $30K-$50K/month. After rent, staff, malpractice insurance, and equipment leases, net margins land at 30-40%.

Cash-pay visits at $65-$85 have 90% margin. Insurance visits at $45-$65 after write-downs have 40-50% margin. Your payer mix is your margin.

The Margin Math

| Approach | Startup Cost | Time Investment | Revenue Potential | Best For |

|---|---|---|---|---|

| Solo operator | Low ($1K-$10K) | Full time | $60K-$200K/yr | Maximum margins, full control |

| Small team (2-5) | Medium ($10K-$50K) | Management + some fieldwork | $200K-$800K/yr | Scaling without losing control |

| DDH Revenue Tracker | Free trial | 5 min setup | N/A (profit tool) | Know your real numbers in real time |

The biggest line item? Rent for a medical-grade office ($3k-$8k/month) and front desk staff ($3k-$4k/month) are fixed costs that don’t scale with patient volume.

Reducing no-show rate from 15% to 5% on 100 weekly appointments adds 10 visits/week — roughly $3K-$4K/month in revenue with zero additional overhead.

What Goes Wrong (and When)

Not tracking patient retention past the initial treatment plan. New patients cost $200-$400 to acquire. If they drop off after 6 visits, your cost per visit is $35-$65. At 30 visits, it’s $7-$13.

January-March spikes from New Year resolutions and new insurance deductibles. Summer dips 10-15%. Auto accident claims increase in winter.

What the Full Dashboard Looks Like

How to Use This Calculator

Start by entering your actual numbers — not estimates. Pull from your bank statements, your POS system, or your accounting software. The difference between estimated and real inputs is usually the difference between “this looks fine” and “oh, that’s where the money is going.”

Then change one variable at a time. For chiropractic practice, the lever that usually moves the needle most is reducing no-show rate from 15% to 5% on 100 weekly appointments adds 10 visits/week — roughly $3k-$4k/month in revenue with zero additional overhead. Start there.

If you want to save these projections, track them month-over-month, or model different scenarios side by side, the full dashboard does all of that. Free 14-day trial, no credit card required.

Your Next Move

Related Tools and Articles

- How to Save $10,000 in 6 Months: A Realistic Plan That Actually Works

- The Complete Guide to Fertility Tracking: Charts, Symptoms & What Your Cycle Is Telling You

- Free PCOS Symptom Tracker Dashboard — Try It Now

Common Questions About I Ran the Numbers on Starting a Chiropractic — Here’s What You’d Make

How long does it take to see results?

Most people see meaningful progress within 30-90 days when they apply these strategies consistently. The key is tracking your numbers from day one so you have a baseline to measure against.

What’s the biggest mistake people make?

Trying to do everything at once. Pick one or two strategies from this guide, implement them fully, then layer in additional tactics. Spreading yourself thin is the fastest way to see no results from any of it.

Do I need special tools or software?

Not necessarily to start — but the right tools eliminate hours of manual work. Our free calculators and trackers at Digital Dashboard Hub are a good starting point before you invest in paid software.

Keep reading (related guides):

255+ interactive tools for your money, time, and health.

Full dashboard access · Stripe-secure checkout · Cancel anytime

What Most People Get Wrong

The single biggest mistake is treating revenue as the headline number. Revenue is vanity — margin is sanity, and cash-in-bank is reality. Two operators with identical top-lines routinely end the year $80K apart in take-home, because one priced for volume and the other priced for sustainability. The calculator above forces you to surface that gap before it hits your bank account.

The second mistake is modeling a “best case” and planning around it. The number you should plan around is the 30th-percentile scenario — enough demand to matter, but slower than you hoped. If the business still covers your living expenses there, you have real margin of safety. If it only works in the 80th-percentile case, you are building on sand.

The third mistake is ignoring your time as a cost. If you would otherwise earn $55/hr at a day job and this operation pays you effectively $18/hr for 60-hour weeks, the gap is the real price of running it. Plug your opportunity cost into the calculator and the picture often flips.

How to Pressure-Test Your Numbers

Start with the calculator, then stress-test three levers independently:

- Pricing: What happens to your take-home if you raise prices 10%, but lose 15% of volume? Most operators are surprised to find net income goes up.

- Costs: What happens if your largest input cost rises 20%? This is not hypothetical — it is a typical 12-month swing in most industries.

- Volume: What happens at 70% of your planned volume for 90 days? If that still covers fixed costs, you have a real business. If not, the model is fragile.

Running the calculator three ways takes about ten minutes. The clarity on the other side of those ten minutes is usually the difference between a confident operating plan and guessing for another six months.

Frequently Asked Questions

How accurate is this calculator?

The underlying math uses industry-standard margin and cost ranges sourced from the I Ran the Numbers on Starting a Chiropractic — Here’s What You’d Make space. Your actual numbers depend on location, seasonality, and operating style, so treat this as a directional benchmark, not a guarantee. The more precisely you enter your inputs, the tighter the output range becomes.

Can I save my results?

A free Digital Dashboard Hub account saves every scenario you run, lets you compare side-by-side, and unlocks the full dashboard with expense tracking and month-over-month charts. The 14-day trial includes the complete tool library — no credit card required to start.

Who is this tool for?

It’s built for anyone pressure-testing a real decision — existing operators auditing their margins, side-hustlers deciding whether to go full-time, and prospective owners trying to sanity-check a business plan before signing a lease. You do not need any accounting background to use it.

What should I do with the results?

Start by comparing the output against your current (or projected) monthly take-home. If the gap is big, walk back the inputs and identify which lever — pricing, volume, or cost structure — is doing the damage. That is usually where the highest-leverage fix lives.

The Bottom Line

Most operators lose money not because the math is impossible, but because they never actually ran it. Fifteen minutes with the calculator beats three months of guessing. Run your numbers, screenshot the output, and use it as the baseline for every pricing and cost decision over the next quarter.

When you are ready to go deeper, the full Digital Dashboard Hub workspace lets you save scenarios, track actuals month-over-month, and see the trend before problems compound. That is the version that actually compounds the effort — spreadsheets forgotten in a Google Drive folder do not.

Next Steps

- Run the calculator above with your best current estimates.

- Re-run it with a pessimistic scenario (lower volume, higher costs) and a stretch scenario (better pricing, more efficient ops).

- Screenshot all three outputs so you have a baseline to compare against when reality arrives.

- Revisit monthly — the number that matters is the one that changes with your real P&L.

Ready for the full dashboard?

Unlock all 255 tools across business, creator, and health workflows.

Andy Gaber is the founder of Digital Dashboard Hub, a suite of 255+ interactive financial, productivity, and wellness tools. He built DDH after getting frustrated with financial apps that gave outputs without context. Follow along for tool tutorials, revenue analytics breakdowns, and honest takes on personal finance.