You’ve heard the advice a thousand times: “You need a budget.” And every time, you nod in agreement, open a spreadsheet, stare at the blank cells for ten minutes, and close the laptop. Budgeting feels overwhelming because most budgeting systems are overwhelming. They want you to track every single dollar across forty-seven categories, reconcile your accounts weekly, and somehow turn yourself into an amateur accountant alongside everything else in your life.

The 50/30/20 rule exists because someone — Senator Elizabeth Warren, actually, in her book “All Your Worth” — recognized that personal budgeting doesn’t need to be complicated to be effective. Three categories. Three percentages. One simple framework that has helped millions of people go from “I have no idea where my money goes” to “I’m in control of my finances.”

But here’s what most articles about the 50/30/20 rule don’t tell you: knowing the rule and implementing the rule are two very different things. You need a system that takes your actual income, your actual expenses, and your actual financial goals and maps them into this framework — then shows you in real time where you stand. That’s what a 50/30/20 budget calculator does, and it’s the difference between understanding the concept and living it.

The 50/30/20 Rule Explained (With Real Numbers)

Let’s break this down with actual math, because percentages are abstract until they become dollar amounts.

The 50%: Needs

Half of your after-tax income goes to needs — the non-negotiable expenses that keep your life running. These are things you literally cannot avoid paying without serious consequences.

What counts as needs:

Housing (rent or mortgage payment, property taxes, homeowner’s insurance), utilities (electricity, water, gas, internet — yes, internet is a need in 2026), groceries (not dining out — actual food you prepare at home), transportation (car payment, insurance, gas, or public transit), minimum debt payments (student loans, credit card minimums, medical debt), health insurance, and childcare if applicable.

What doesn’t count: Your Netflix subscription, dining out, gym membership, or that premium Spotify plan. Those feel like needs, but they’re wants. Be honest with yourself here — the accuracy of your budget depends on it.

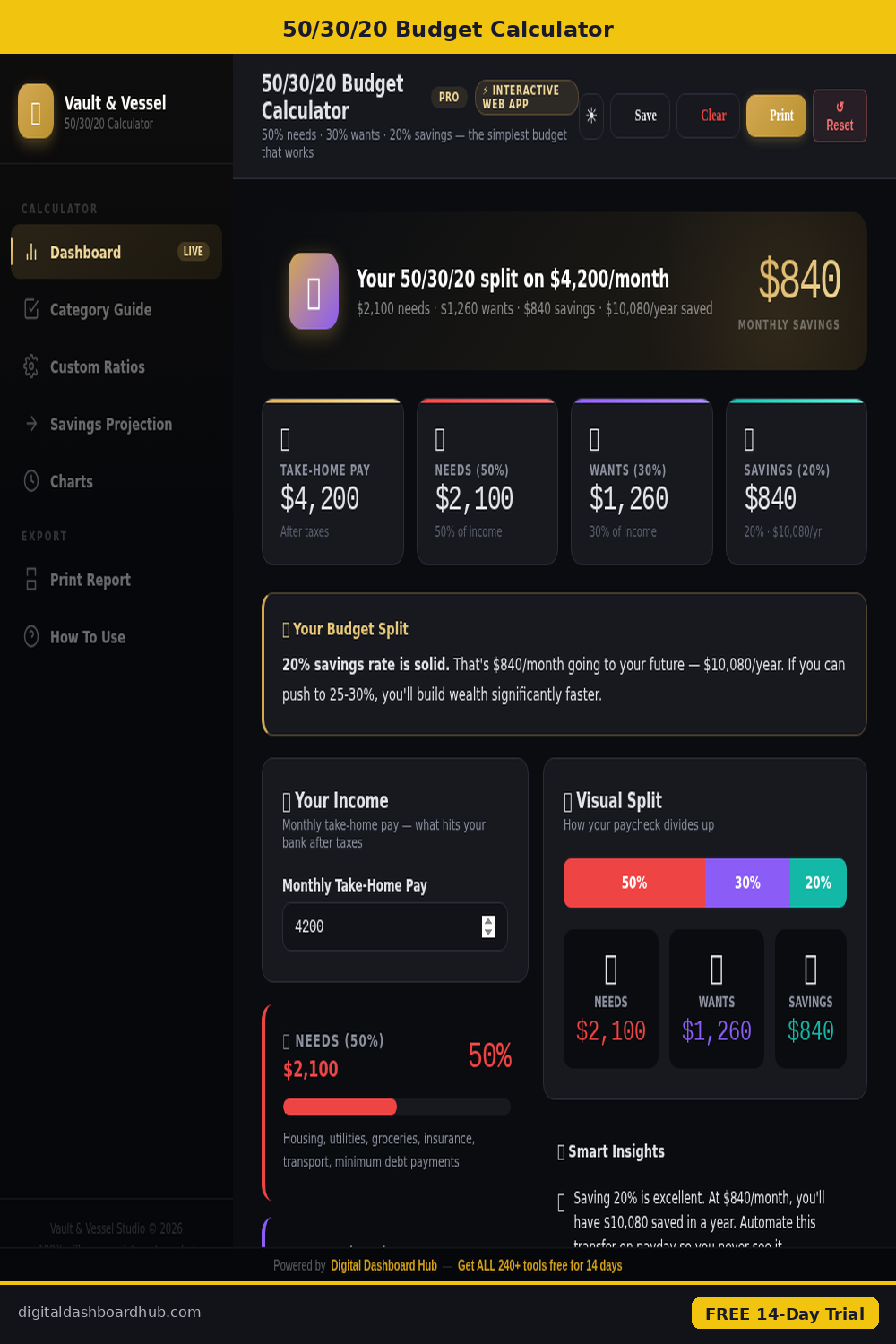

Example: If your after-tax monthly income is $5,000, your needs budget is $2,500. If your rent alone is $2,200, you immediately see the problem — and the calculator helps you see it in stark numerical terms rather than a vague feeling of “things are tight.”

The 30%: Wants

Thirty percent goes to wants — the things that make life enjoyable but that you could technically live without. This is the category most people either overspend on (without realizing it) or feel guilty about (unnecessarily).

What counts as wants: Dining out and takeout, entertainment (streaming services, movies, concerts, events), shopping (clothing beyond basics, electronics, home decor), hobbies and recreation, gym membership, travel and vacations, personal care beyond basics (haircuts count; fancy salon treatments are wants), and subscription services.

The beautiful thing about the 50/30/20 rule is that it explicitly gives you permission to spend 30% of your income on things you enjoy. You don’t need to feel guilty about buying a coffee or going out to dinner — as long as it fits within your 30%.

The 20%: Savings and Debt Payoff

Twenty percent goes to your financial future. This is the money that builds your safety net, pays off debt faster, and grows your wealth over time.

What counts: Emergency fund contributions, retirement account contributions (beyond employer match), extra debt payments (above the minimum), investment contributions, and savings for specific goals (house down payment, car fund, education fund).

Example: On a $5,000 after-tax income, that’s $1,000 per month going toward your financial future. Over a year, that’s $12,000. Over five years with modest investment returns, that’s over $70,000. The 20% doesn’t feel dramatic month to month, but its compounding effect is life-changing.

Why the 50/30/20 Rule Works When Other Budgets Fail

Simplicity Reduces Decision Fatigue

Traditional line-item budgets require you to make dozens of spending decisions: “Am I over budget in the ‘personal care’ category? What about ‘household supplies’? Wait, does this cleaning product count as ‘household supplies’ or ‘grocery’?” This cognitive overhead is exactly why most budgets get abandoned.

The 50/30/20 rule asks you three questions. Three. That’s it. Is this a need, a want, or savings? Every spending decision fits into one of three buckets. Your brain can handle that.

Flexibility Prevents Rebellion

Rigid budgets that allocate $47.50 to “coffee” and $125 to “clothing” are brittle. One unexpected expense shatters the whole system. The 50/30/20 approach gives you large buckets with internal flexibility. If you spend less on dining out this month, you can spend more on a concert without blowing your budget. As long as total wants stay under 30%, you’re good.

It Scales With Income Changes

Got a raise? Your budget automatically adjusts. Lost overtime? Same thing. Because the framework is percentage-based, it works at any income level. The specific dollar amounts change, but the ratios stay constant. This means you don’t have to rebuild your budget every time your income fluctuates.

How to Set Up Your 50/30/20 Budget (Step-by-Step)

Step 1: Calculate Your After-Tax Income

This is your starting number. If you’re a salaried employee, this is your net pay (the number on your paycheck after taxes, health insurance, and retirement contributions are deducted). If you’re self-employed or freelance, calculate your average monthly income after setting aside money for taxes (typically 25-30% for self-employment).

Important: If your employer deducts retirement contributions from your paycheck, add those back in before calculating your 20%. Those contributions count toward your savings category.

Step 2: List and Categorize Your Current Spending

Pull your last three months of bank and credit card statements. Categorize every transaction as a Need, Want, or Savings/Debt payment. Three months gives you a reliable average — one month can be skewed by irregular expenses.

This step is where most people have their “oh” moment. You think you know where your money goes. You don’t. The data always reveals surprises: the subscription services you forgot about, the dining-out spending that’s triple what you estimated, the “small” purchases that add up to hundreds.

Step 3: Compare Reality to the 50/30/20 Targets

Now compare your actual spending ratios to the ideal. Most people find something like 65/30/5 or 55/35/10. The gap between where you are and where you want to be becomes your roadmap.

Step 4: Identify Your Adjustment Levers

If your needs exceed 50%, you have structural spending that requires either income growth or major changes (downsizing housing, refinancing debt, reducing transportation costs). These aren’t quick fixes, but they’re the highest-impact ones.

If your wants exceed 30%, look for the low-hanging fruit: unused subscriptions, dining-out frequency, impulse purchases. These adjustments can often be made immediately.

Try Our Free Finance Dashboard

Track your numbers automatically with our interactive cloud dashboard. No spreadsheet skills needed.

If your savings are below 20%, automate the increase. Set up automatic transfers to savings on payday, before you have a chance to spend the money. Start with whatever you can — even 5% — and increase by 1% each month until you hit 20%.

Step 5: Automate and Track

The final step is building a system that runs with minimal effort. Automate your savings transfers. Set up spending alerts when you approach category limits. And use a calculator that shows you in real time where you stand against your 50/30/20 targets.

Common 50/30/20 Challenges (And How to Solve Them)

“My Rent Takes Up More Than 50% of My Income”

This is the most common challenge, especially in high-cost-of-living areas. If your needs genuinely exceed 50%, you have a few options: adjust the ratio temporarily (like 60/20/20) while you work on increasing income or reducing fixed costs, look for ways to reduce other needs (lower insurance premiums, refinance student loans, reduce utility costs), or consider whether any of your “needs” are actually wants (that car payment for a new vehicle when a used one would work, for example).

“I Don’t Know If Something Is a Need or a Want”

Apply the “consequence test.” If you stopped paying for it, what would happen? If the consequence is serious (eviction, no transportation to work, hunger), it’s a need. If the consequence is inconvenience or reduced enjoyment, it’s a want. Groceries are a need. Organic artisanal groceries at twice the price contain a want premium.

“I Have Irregular Income”

Freelancers, gig workers, and commission-based earners need a modified approach. Calculate your average monthly income over the past twelve months. Use that average as your budget baseline. In high-earning months, bank the excess. In low-earning months, draw from the buffer. The percentages stay the same — the base number just smooths out.

“I’m Drowning in Debt”

If your minimum debt payments alone push needs past 50%, consider a temporary modified ratio like 50/20/30 where the extra 10% from wants goes to accelerated debt payoff. Once your debt is under control, transition to the standard 50/30/20.

Using a Digital Calculator to Stay on Track

A spreadsheet can handle basic 50/30/20 math, but a purpose-built calculator offers significant advantages. It automatically categorizes transactions, calculates your real-time ratios, projects forward based on current spending trends, and alerts you when you’re drifting off target.

The 50/30/20 Budget Calculator on Digital Dashboard Hub does all of this in an interactive dashboard. Enter your income, plug in your expenses, and instantly see where your money goes versus where it should go. The visual breakdown makes the abstract percentages concrete — and concrete numbers drive concrete changes.

The gap between “I should budget” and “I am budgeting” is smaller than you think. It starts with one calculation.

Ready to see where your money actually goes? Try the 50/30/20 Budget Calculator free for 14 days at digitaldashboardhub.com/trial — no credit card required. Your finances won’t organize themselves, but they can organize themselves a lot faster with the right tool.

Related articles: How to Budget on a Biweekly Paycheck, Zero-Based Budgeting: How to Give Every Dollar a Job, How to Save $10,000 in 6 Months

Get Free Finance Tools & Resources

Join our newsletter for exclusive templates, calculators, and expert tips delivered weekly.

Disclaimer: This article is for informational purposes only and does not constitute professional advice. Always consult with a qualified professional for your specific situation.