Introduction: The Reality Check Nobody Gave You

Before you scroll: the calculator below is running in your browser right now. For the full feature set — saved scenarios, history, exports — open the dashboard.

You got your acceptance letter. You picked out your dorm supplies. You imagined yourself thriving at college, making friends, acing exams, and maybe—just maybe—still having money left over for pizza on Friday night.

Then reality hit. Your tuition bill arrived. Your first month of rent felt like a gut punch. And you looked at your bank account wondering how you were supposed to survive until graduation without eating ramen every single day (okay, maybe some days).

Here’s the thing: nobody really talks about the actual money side of college. We talk about GPAs, networking, and choosing the right major, but we skip right past the part where you’re genuinely stressed about affording textbooks AND basic groceries. That ends today.

This guide isn’t about achieving some perfect, Pinterest-worthy budget. It’s about the real money stuff that college students actually face—and how to navigate it without drowning in debt before you even graduate.

Part 1: The Real Cost of College (And We’re Not Just Talking Tuition)

Let’s break down what a college budget actually looks like. Your expenses probably fall into these categories:

-

Tuition and fees (varies wildly depending on school)

-

Housing (dorm, apartment, or back home with parents)

-

Food (meal plan, groceries, that coffee you swear you don’t drink daily)

-

Textbooks (outrageously expensive, by the way)

-

Phone bill and internet

-

Transportation (gas, parking, public transit, or that bike you bought and never used)

-

Utilities (if you’re in an apartment)

-

Health insurance and medical expenses

-

Clothing and personal care items

-

Streaming subscriptions you share with four friends but still get charged for

-

Coffee runs (seriously, track this)

-

Eating out because cooking is hard

-

Drinks on Friday night

-

Concert tickets, movies, and social activities

The uncomfortable truth? You probably have way more expenses than your financial aid covers. And that’s not a personal failure—it’s just reality.

Part 2: Where the Money Actually Comes From

| Method | Time to Set Up | Accuracy | Automation | Best For |

|---|---|---|---|---|

| Spreadsheet (manual) | 2-4 hours | High (if maintained) | None | Detail-oriented budgeters |

| Budget apps (Mint/YNAB) | 30-60 min | Medium (syncing errors) | Bank sync | Hands-off tracking |

| DDH Financial Dashboard | 5-10 min | High (you control inputs) | Interactive calculator | Freelancers, variable income, small business owners |

Before you can budget, you need to know what you’re working with. Your income as a college student likely comes from multiple places:

If you’re getting grants or scholarships—congratulations, this is the best kind of money because you don’t pay it back. Federal student loans? Well, those you do have to repay. The key is understanding exactly what you’re getting and when. Financial aid doesn’t always arrive on your schedule, which is why this matters.

Most college students work part-time. Some balance 10 hours a week; others work 30. There’s a reason for the “don’t work more than 20 hours per week” recommendation—studying actually matters for your degree. But some students need to work more just to survive. That’s okay. Just be realistic about how much you can actually earn while maintaining your grades.

Maybe your parents send money. Maybe they don’t. There’s no shame either way. But if this is part of your budget, account for it realistically—and don’t assume it’ll always be there.

Some students come to college with savings or pick up occasional gigs (tutoring, freelance work, selling class notes… okay, don’t do that last one). These are bonus money, not something to depend on.

Part 3: Building Your Actual Student Budget (Not the Fake One)

Here’s where we get practical. Creating a college budget spreadsheet doesn’t have to be complicated, but it does have to be honest.

Add up everything coming in during a semester. Include financial aid, loans, your job income, and family help. This is your total budget.

These are the things you can’t skip: tuition, housing, minimum required food, insurance. These usually take up 60-70% of your budget. And yes, if you’re taking out student loans, factor in that you’ll eventually need to repay them—even if that feels like someone else’s problem right now.

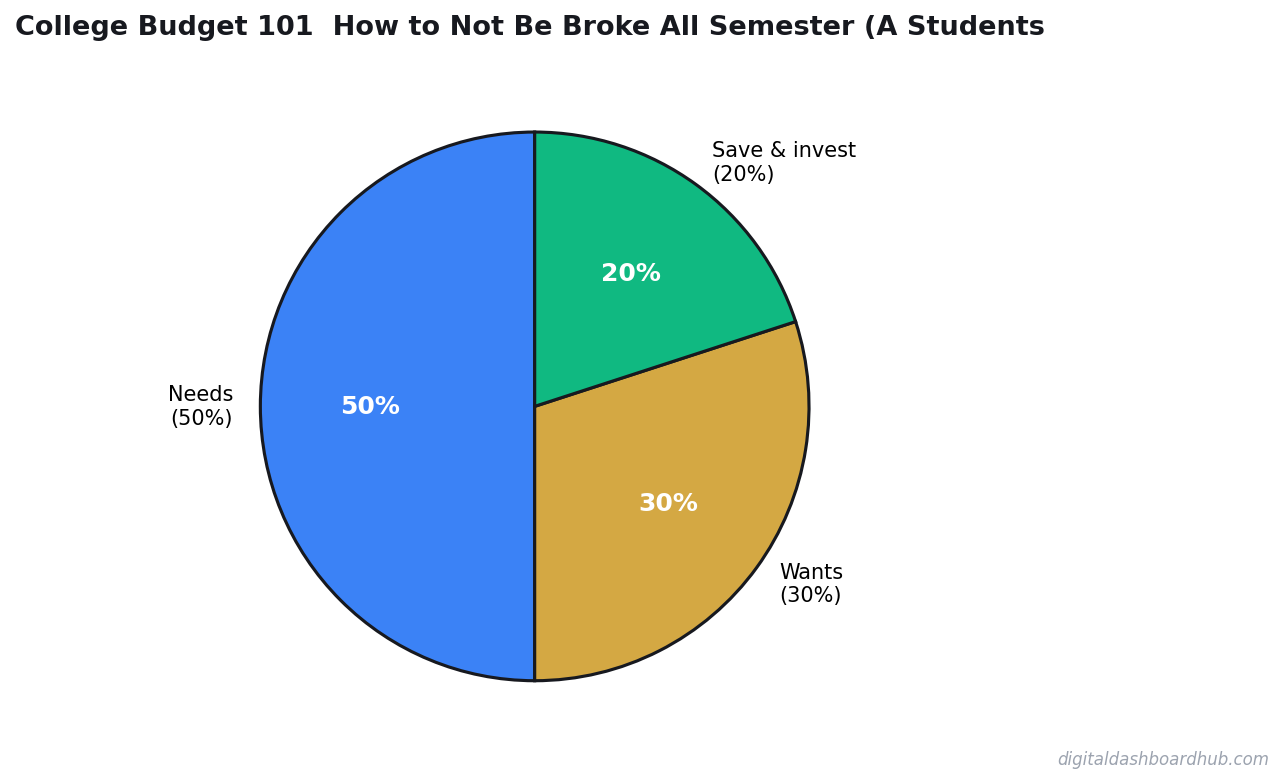

The popular 50/30/20 rule (50% needs, 30% wants, 20% savings) doesn’t really work for college students making tight money. Instead, try a modified version that accounts for reality:

- 60-70% on non-negotiables (housing, tuition, food, insurance)

- 15-20% on variable needs (transportation, phone, personal care)

- 10-15% on wants (entertainment, eating out, subscriptions)

- 5-10% on savings (even if it’s tiny, consistency matters)

If your math doesn’t add up and you’re short, that’s when you make tough choices. Can you reduce housing costs? Work a few extra hours? Buy cheaper textbooks (used or rental)? Skip the meal plan and cook? These conversations are uncomfortable but necessary.

Pro Tip: Use a simple spreadsheet or a dedicated tool. Our Monthly Budget Planner is specifically designed for students and breaks down exactly where your money goes. If you get paid biweekly, this Biweekly Budget Template might serve you better. Knowing your exact numbers is the foundation of not being broke all semester.

Part 4: The Debt Traps Every College Student Should Avoid

Student debt is tricky because some of it (federal student loans) is sometimes necessary, but other debt? That’s a choice. Here’s what to watch out for:

Credit cards aren’t evil, but they’re dangerous for college students. Especially when you’re already tight on money. The interest rates are brutal, and it’s way too easy to think of a credit card as “free money.” It’s not. It’s borrowed money with interest, and if you carry a balance, you’re paying extra for everything you buy. Don’t let a $20 coffee cost you $30 by the time you pay it off.

Here’s what happens: You get a part-time job and suddenly feel rich. You upgrade your meal plan, start ordering food instead of cooking, buy new clothes just because. Then you depend on that spending level and scramble when you don’t work extra hours. Keep your lifestyle at the level of your baseline budget. Extra income goes to savings, not lifestyle upgrades.

If you’ve exhausted federal aid and federal loans, private loans are tempting. But they usually have worse terms, fewer protections, and higher interest rates. Exhaust federal options first. Talk to your financial aid office about other options before going private.

Some students rack up debt for non-essentials—spring break trips, new electronics, brand-name everything. The hard truth: you can’t afford these right now. Not because you’re bad with money, but because you’re a student. This is temporary. Living below your means now means graduating with less debt, which means having more financial freedom later.

Part 5: Money-Saving Hacks That Actually Work

You’ve built your budget, and it’s tight. Here’s how to stretch every dollar:

New textbooks can cost $150+ each. Solve this by: buying used, renting, checking if your library has copies, seeing if classmates will split an access code, or using older editions. Some professors don’t even require the textbook—ask first.

Meal plans aren’t always the cheapest option. If you can cook, buy groceries in bulk, meal prep on Sundays, and skip the daily coffee runs. Cook with friends to split costs. Shop sales and use generic brands. This alone might save you $50-100 per month.

If you’re paying for housing, this is where to negotiate. Roommates split costs. Living off-campus might be cheaper than dorms. Some students go home for summers to save money. Explore all options.

Walk when possible. Use public transit passes designed for students. Carpool. Bike. These small changes add up.

Do you actually use Netflix, Disney+, Spotify, and gym membership? Probably not. Kill what you’re not actively using. Share streaming accounts with family (it’s usually allowed).

If you want to automate your savings without thinking about it, check out this 50/30/20 Budget Calculator—it helps you visualize exactly where money should go so you stop wondering where it disappeared to.

Part 6: The Emergency Fund (Yes, Even as a Student)

I know, I know. You’re barely making it work. How can you save?

Start small. Even $10-20 per month adds up. An emergency fund—even a small one—is the difference between a car repair being an inconvenience versus a full-blown crisis that requires new debt.

Aim for at least $500-1,000 by the end of your first year. This covers most unexpected expenses without derailing your budget. If the thought of saving feels impossible, use this Emergency Fund Calculator to figure out realistic targets based on your actual income.

Part 7: If You’re Already in Debt (It’s Not Too Late)

Maybe you’re reading this and you’re already carrying credit card debt or looking at a loan balance and feeling sick. First: breathe. You’re not alone, and it’s fixable.

Make a list of all your debt: What do you owe? What’s the interest rate? Minimum payment?

Stop creating new debt while you’re paying off old debt. This is non-negotiable.

Prioritize your debt: Pay minimums on everything, then throw extra money at the highest interest rate debt first (avalanche method) or the smallest balance first (snowball method—it feels better psychologically).

If you’re weighing different strategies, this Debt Snowball vs Avalanche Simulator shows you exactly which approach saves you the most money. And once you have a payoff plan, this Debt Payoff Tracker keeps you motivated by showing progress.

The Bottom Line: You’ve Got This

College is expensive. Your budget will be tight. You will sometimes have to choose between new shoes and groceries—and that sucks. But this season of your life is temporary. Every dollar you don’t borrow now is money you’re not paying interest on for years after graduation.

Your future self will thank you for making hard choices today.

Start with a simple budget spreadsheet. Track where your money actually goes (not where you think it goes). Make tough choices about what’s essential. Avoid debt traps. Save what you can. And remember: being broke in college is normal. What matters is being intentional about your money instead of just letting it disappear.

Ready to Take Control of Your Student Budget?

Creating a budget is one thing. Sticking to it is another. That’s why we created tools specifically for students and people just starting their financial journey.

If you need a simple way to track your money across the semester, start with this Monthly Budget Planner—it’s designed to handle paychecks, financial aid, and all those unexpected expenses.

Want to understand exactly where each paycheck should go? The Paycheck Breakdown Analyzer removes the guesswork and shows you exactly what to allocate to each category.

Or if you work cash jobs or prefer physical money, our Cash Envelope Budget system combines digital tracking with real accountability.

Download our free College Semester Budget Planner to get started today. Enter your email below, and we’ll send you a simple template you can customize for your exact situation. No spam. No up-selling. Just practical tools to help you make it through the semester without panic.

[Email Capture Box: “Get Your Free College Budget Planner” with email field]

Your future self is waiting for you to make this choice. Start today.

About Vault & Vessel Studio: We create real-world budgeting tools for real people. Our Google Sheets templates help college students, freelancers, and anyone tired of financial chaos take back control. Learn more at vaultandvesselstudio.com.

Keep Reading

- I Tested 9 Expense Tracker Apps for 3 Months — Here’s What Actually Worked

- Freelancer Finance Management Dashboard (VVS): Finally, a Money Tool Built for Variable Income

- Airbnb Revenue Calculator: Estimate Your Short-Term Rental Income Before You List

Keep reading (related guides):

- Business Expense Tracker: Categorize and Export for Tax Time

- How Much Money You Need to Retire Early at 40, 45, and 50 (Real Numbers by Age)

- Best Wedding Budget Planner: The Only Tool That Covers All 27 Categories

- Savings Rate Calculator: The One Number That Predicts Your Financial Future

- Amazon FBA Revenue Calculator: What Sellers Actually Make in 2026

255+ interactive tools for your money, time, and health.

Full dashboard access · Stripe-secure checkout · Cancel anytime

Andy Gaber is the founder of Digital Dashboard Hub, a suite of 255+ interactive financial, productivity, and wellness tools. He built DDH after getting frustrated with financial apps that gave outputs without context. Follow along for tool tutorials, revenue analytics breakdowns, and honest takes on personal finance.