So I built a house hacking calculator that runs the math for your specific situation — your income, your tax bracket, your timeline. No generic advice. Just your numbers.

The Real Math Behind House Hacking

The dashboard below loads instantly in your browser. Plug in your numbers, see your answer. No signup to try the basics.

Here’s why most people get house hacking wrong: they focus on one variable and ignore three others. The decision depends on your current tax bracket, your expected retirement tax bracket, your investment timeline, and your state tax situation. Change any one of those and the “right” answer flips.

The conventional wisdom says pick one approach and stick with it. The data says something different: the right strategy changes as your income changes. What worked when you made $60K might cost you thousands at $120K. That’s where a good calculator earns its keep. For more on getting your financial foundation right, see Freelance Tax Planner: Stop Overpaying the IRS (Free Calculator).

3 Mistakes That Cost People Thousands

Mistake #1: Ignoring state taxes. If you live in a state with no income tax and plan to retire in one that does (or vice versa), the calculation shifts dramatically. A $500K portfolio difference over 30 years isn’t unusual.

Mistake #2: Assuming your tax bracket won’t change. Most people’s income peaks between ages 45-55. Planning your entire house hacking strategy based on your 28-year-old income is leaving money on the table.

Mistake #3: Not running the numbers at all. This is the biggest one. People spend more time researching their next phone purchase than the financial decision that will affect them for 30+ years.

How the DDH House Hacking Calculator Handles This

Here’s what actually using this calculator looks like.

Step 1: Enter your current income, filing status, and state. The tool pulls in the correct federal and state tax brackets automatically.

Step 2: Set your contribution amount and timeline. The calculator runs compound growth with realistic return assumptions (not the 12% fantasy numbers some advisors use).

Step 3: Compare scenarios side by side. See the difference in after-tax wealth at 5, 10, 20, and 30 year intervals. The visualization makes the decision obvious.

The piece that makes this different from the 50 other calculators online: it shows you the crossover point — the exact year where one strategy beats the other for your specific situation. For most people, that number is surprising.

Try it yourself: Open the House Hacking Calculator free → — 14-day trial, no credit card required.

DDH Calculator vs Alternatives

| Feature | Bankrate/NerdWallet | Financial Advisor | DDH Tool |

|---|---|---|---|

| State tax accuracy | Limited | Yes | Yes |

| Side-by-side comparison | No | Varies | Built-in |

| Cost | Free (with ads) | $200-500/session | Free trial |

| Multiple scenarios | Run separately | 1-2 max | Unlimited |

Your Next Move

Right now (2 minutes): Look up your current marginal tax rate. If you don’t know it off the top of your head, that tells you something.

This week: Pull your last pay stub and check what you’re currently contributing. Calculate the annual total. Is that number intentional or just whatever you set when you first got the account?

The long play: Run your numbers through the DDH House Hacking Calculator. Free for 14 days, no credit card. You’ll see exactly how your current strategy compares to the alternatives — and whether a switch could save you thousands. It’s one of 255+ financial tools on the platform.

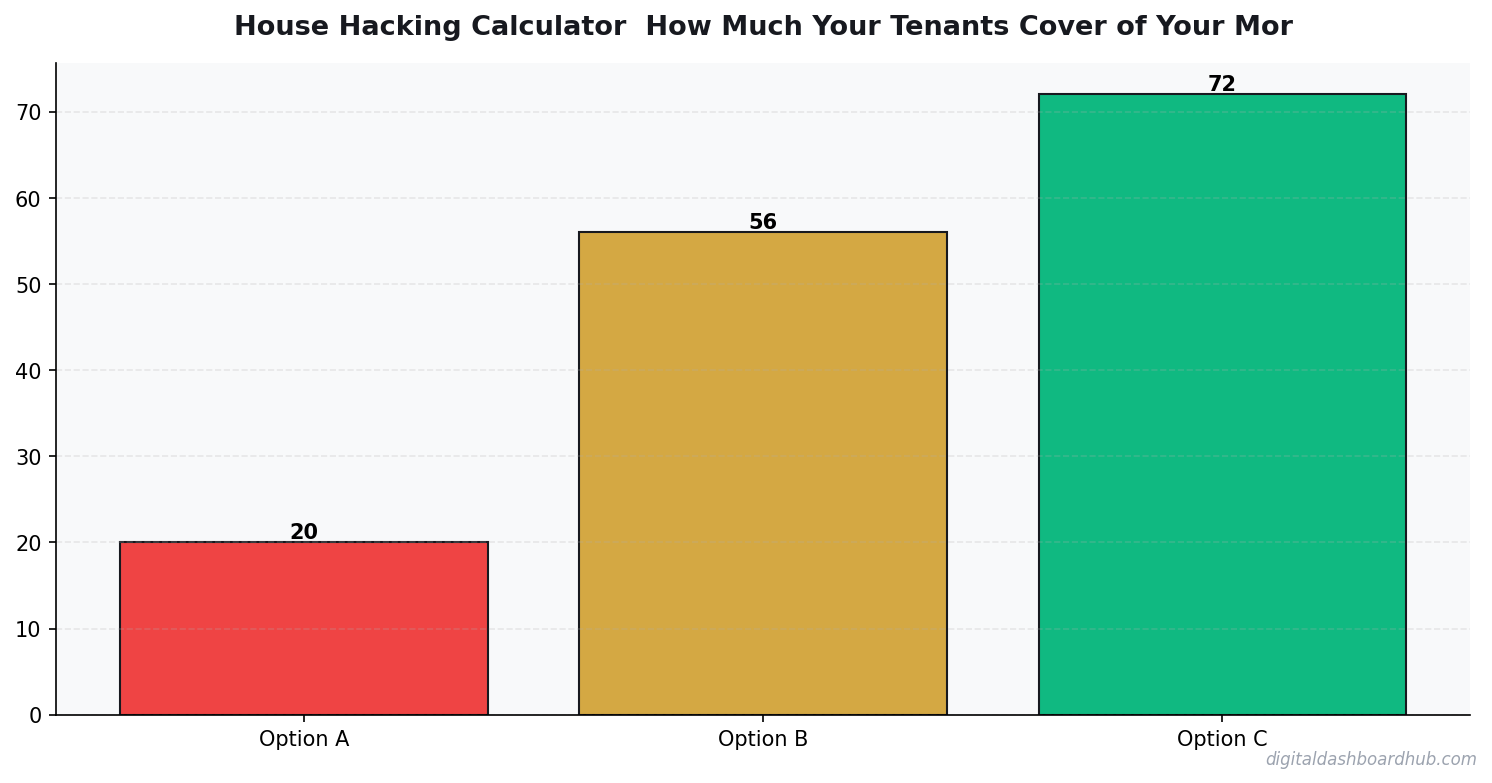

A Real House Hack: What the Numbers Look Like

A buyer purchases a duplex in Columbus, OH for $285,000 with 5% down (FHA). Total mortgage PITI: $2,150/month. They live in unit 1. Unit 2 rents for $1,275/month. After 5% vacancy reserve: effective rental income $1,211/month.

Net housing cost: $2,150 – $1,211 = $939/month. Comparable single-family rent in the same neighborhood: $1,600/month. Monthly savings: $661. Over 5 years, the house hacker accumulates ~$85,000 in equity while paying effective “rent” of $900–$950/month. The pure renter spent $100,000+ and has nothing.

The Two Scenarios People Forget to Model

Optimistic case: You house-hack a triplex with two units renting at $1,100 each. Mortgage: $2,400. Net cost: $200/month. Effectively living for free while tenants pay down your mortgage. This happens in mid-tier markets where triplex prices haven’t been bid up by institutional investors.

Pessimistic case: Your tenant stops paying. Ohio eviction process: 45–90 days minimum. During that window, you’re covering the full mortgage. Always model assuming 2–3 months of zero rental income per year. If the math still works, you have a real deal. If it only works at 100% occupancy, one difficult tenant becomes a financial crisis.

What Most First-Time House Hackers Get Wrong

Underestimating landlord responsibilities. When you live next to your tenant, every maintenance call is personal and immediate. Expect 4–8 hours of landlord work per month. If you’ll resent that, hire a property manager at 8–10% of rent — and rerun the numbers with that cost included.

Also: the FHA owner-occupancy requirement. FHA loans require you to live in the property for at least 1 year. After that, you can move out and convert to a full rental. The year-one house hack is also a trial period for being a landlord — useful information before you commit to an investment-only property with no built-in exit.

Keep reading (related guides):

- Rent vs. Buy Calculator 2026: The True Cost of Each Option (Real Numbers)

- True Cost of Your Mortgage Calculator: Its More Than the Payment

- Working From Home With ADHD: The Complete Setup Guide

- Mortgage Comparison Calculator: Find the Best Rate and Term

- Amazon FBA Revenue Calculator: What Sellers Actually Make in 2026

255+ interactive tools for your money, time, and health.

Full dashboard access · Stripe-secure checkout · Cancel anytime

Questions people ask before using this tool

Is a House Hacking better than a financial advisor?

For the decision this tool handles, usually yes — you can see the math in 30 seconds instead of scheduling a meeting. For comprehensive planning across taxes, estate, and insurance, an advisor still earns their fee. Use tools like this to pre-decide obvious cases, then bring harder ones to a human.

Can a House Hacking handle my situation if I am self-employed?

Partially. The core math works the same — the blind spot is self-employment tax, SEP/Solo 401(k) limits, and quarterly estimated payments. Treat the calculator as 80% of the answer and confirm the self-employment specifics with a CPA before the final move.

What is the biggest mistake first-time users of a House Hacking make?

Plugging in their current number and stopping there. The value is running scenarios — what if income goes up 20%, what if they contribute an extra $200/month, what if they retire 3 years later. The calculator is a ‘what if’ engine, not a one-shot snapshot.

What numbers do I need before using a House Hacking?

Current income, marginal tax bracket, existing balance or equity, expected annual contribution, and a time horizon. If you are missing one, use the default — the tool shows you which inputs move the output most, so you can refine the one that matters.

How accurate is the output of a House Hacking?

As accurate as your inputs. The calculator uses standard formulas — where it can get wrong is the assumption layer (tax bracket, state, employer match, future contribution rate). Run it three times with conservative, base, and optimistic assumptions to see the range of outcomes.

Should I re-run the House Hacking every year?

Yes. Tax brackets, income, goals, and market conditions change annually. A 30-minute re-run every January is cheaper than the mistake of assuming last year’s math still applies. Most users find their optimal allocation shifts meaningfully every 3-5 years.

Seven mistakes to avoid with this House Hacking tool

- Ignoring tax drag. A House Hacking that skips the tax line gives you a fantasy number; your real take-home lives on the other side of the bracket.

- Optimizing for the wrong time horizon. A decision that looks great at 5 years may lose at 20; always re-run at multiple horizons.

- Not factoring in fees. A 0.5% fee looks small; over 30 years it is often 15-20% of your ending balance. Re-run with realistic expense ratios.

- Anchoring on employer defaults. The default contribution rate is set for the company’s benefit, not yours — always check the math yourself.

- Running the House Hacking once and treating the output as gospel. Every major life change (income, marriage, move) invalidates the last result.

- Skipping the ‘what if the market returns 4% instead of 7%’ run. Recessions are baked into long-term math — your plan should survive them.

- Comparing account types one at a time. The right move is usually a blend; run the tool three times and compare side-by-side.

Tools like this House Hacking are only as useful as the habit of re-running them. A one-shot calculation at the start of the year rarely survives contact with the market; a 15-minute quarterly refresh beats a one-hour annual audit.

When to use this House Hacking tool (and when to skip it)

This House Hacking tool is most valuable at three decision points: a major income change (raise, job switch, self-employment jump), a planned big expense or investment (home purchase, refinance, business buy-in), and the annual tax-planning window in October-December. Run it at those moments and the outputs directly inform actions you are about to take anyway.

Skip the tool for small, reversible decisions — whether to adjust a monthly contribution by $50, for example, rarely moves a long-horizon projection enough to justify the modeling time. Also skip it for tax-year-specific edge cases like estate planning, complex stock options, or international moves; those require an advisor with access to your full situation, not a generic calculator.

Smart users treat calculators as a ‘what if’ playground, not a prescription. Run the same scenario three different ways — conservative, baseline, aggressive — and you will learn more from the spread than from any single output. That spread is where the real decision lives.

House Hacking quick reference checklist

Before you lock in a decision based on the House Hacking, walk this checklist one more time.

- You know which single input moves the output the most, and you are confident in that number.

- You compared at least two paths side-by-side, not one number in isolation.

- You factored fees, taxes, and inflation — not just the headline return.

- You ran the numbers at least three times with different assumption sets.

- You checked what happens if market returns are 3-4% instead of the baseline 7%.

- You wrote down the inputs, so you can re-run next year and see what actually moved.

What to do next

Once you have walked the checklist, scroll back up and run your real inputs in the interactive House Hacking tool — it takes about 60 seconds. If you want to compare this against the other 254+ calculators, trackers, and planners in the DDH library, the full set lives at app.digitaldashboardhub.com. Free tier covers the core version of every tool; upgrades unlock cross-tool dashboards, scenario saving, and team sharing.

If you are brand new to the DDH toolkit, start with three tools: one that directly serves your primary goal this quarter, one that catches problems before they compound, and one just for fun. That mix prevents the usual fate of productivity tools — great first month, forgotten by month three.

Keep Reading

- Freelance Tax Planner: Stop Overpaying the IRS (Free Calculator)

- Freelance Quote Builder: Stop Undercharging (Free Calculator)

- Airbnb Revenue Calculator: How to Estimate Your Rental Income Before Buying

- How Much Does a Hair Salon Make? (2026 Revenue Calculator)

Common Questions About House Hacking Calculator: How Much Your Tenants Cover of Your Mortgage

How long does it take to see results?

Most people see meaningful progress within 30-90 days when they apply these strategies consistently. The key is tracking your numbers from day one so you have a baseline to measure against.

What’s the biggest mistake people make?

Trying to do everything at once. Pick one or two strategies from this guide, implement them fully, then layer in additional tactics. Spreading yourself thin is the fastest way to see no results from any of it.

Do I need special tools or software?

Not necessarily to start — but the right tools eliminate hours of manual work. Our free calculators and trackers at Digital Dashboard Hub are a good starting point before you invest in paid software.

Andy Gaber is the founder of Digital Dashboard Hub, a suite of 255+ interactive financial, productivity, and wellness tools. He built DDH after getting frustrated with financial apps that gave outputs without context. Follow along for tool tutorials, revenue analytics breakdowns, and honest takes on personal finance.