Your $350,000 House Will Cost You $750,000 — And That’s the Optimistic Number

I launched Digital Dashboard Hub because the tools I found online were either too generic or too complicated. Here’s the honest breakdown:

When your lender approved you for a $2,100/month mortgage, you probably thought, “I can handle that.” What nobody showed you was the other $400,000 you’ll pay over 30 years in interest, insurance, taxes, maintenance, and the invisible cost of tying up your down payment. The monthly payment is the tip of the iceberg, and the iceberg sinks more household budgets than any other single expense.

I bought my first house thinking I understood the costs. I was off by about $180,000 over the life of the loan. Here’s the full picture so you don’t make the same mistake.

The Full Cost Breakdown of a $350,000 Home

Let’s use a realistic 2026 scenario: $350,000 purchase price, 20% down ($70,000), 6.75% interest rate, 30-year fixed mortgage.

*Adjusted for estimated annual increases.

Total true cost: $1,161,320 — $1,291,320 (with HOA). For a house listed at $350,000. That’s 3.3x to 3.7x the sticker price.

The Cost Nobody Puts in the Spreadsheet: Opportunity Cost

That $70,000 down payment? If you’d invested it in a broad market index fund averaging 8% annually over 30 years, it would grow to roughly $703,000. The opportunity cost — what you gave up by tying that money to a house — is over $630,000 in foregone growth.

Now, your house will also appreciate. Historically, real estate appreciates at about 3.5-4% annually nationally. A $350,000 home might be worth $980,000-$1,120,000 in 30 years. But you have to subtract all the costs above to find your real return. And you can’t spend your house’s appreciation without selling it or borrowing against it.

Interest: The Silent Majority of Your Payment

In the first year of a 30-year mortgage at 6.75%, about 77% of every payment goes to interest. You’re paying $1,400/month in interest and only $417 toward actually owning the house. It takes about 20 years before the split flips and more goes to principal than interest.

Here’s how the interest-to-principal ratio changes over time:

How to Reduce Your True Cost by $100K+

These are the highest-impact moves, ranked by dollar savings:

- Make one extra payment per year: Cuts ~4-5 years off your loan and saves $80,000-$120,000 in interest on a $280K mortgage.

- Refinance if rates drop 0.75%+ below your current rate: On the loan above, dropping from 6.75% to 6.0% saves roughly $55,000 over the remaining term (break-even in ~18 months on closing costs).

- Skip PMI entirely: Put 20% down or use a piggyback loan. PMI on a $350K house with 10% down costs about $150/month — that’s $18,000+ before you hit 20% equity.

- Shop insurance annually: Most people set-and-forget their homeowners insurance. Getting 3 quotes each renewal can save $300-$800/year — up to $24,000 over 30 years.

Ready to see your real numbers? Our true cost of mortgage calculator maps out every category — interest, taxes, insurance, maintenance, and opportunity cost — for your specific purchase price, rate, and down payment. It’s the spreadsheet your lender will never show you.

The Question You Should Really Be Asking

It’s not “can I afford the monthly payment?” It’s “what is the total cost of ownership over my expected time horizon, and does that beat renting + investing the difference?” Sometimes buying wins. Sometimes it doesn’t. But you can’t know unless you see the full picture.

A house is still the right move for many people — forced savings, stability, and the psychological benefit of ownership are real. Just don’t make a $750,000 decision based on a $2,100/month number.

Do This First

- Right now: Pull up your most recent mortgage statement (or your pre-approval letter) and note the principal, interest rate, and current balance. That’s your starting point.

- This week: Run your numbers through a true cost calculator that includes property tax, insurance, maintenance, and opportunity cost — not just P&I.

- Long game: Set up biweekly payments instead of monthly. You’ll make 26 half-payments per year (13 full payments) instead of 12, saving tens of thousands in interest without feeling the pinch.

More than 950 homebuyers have used our mortgage analysis tools this quarter. The most common reaction? “I had no idea interest was that much.” Now you do. See your full cost breakdown.

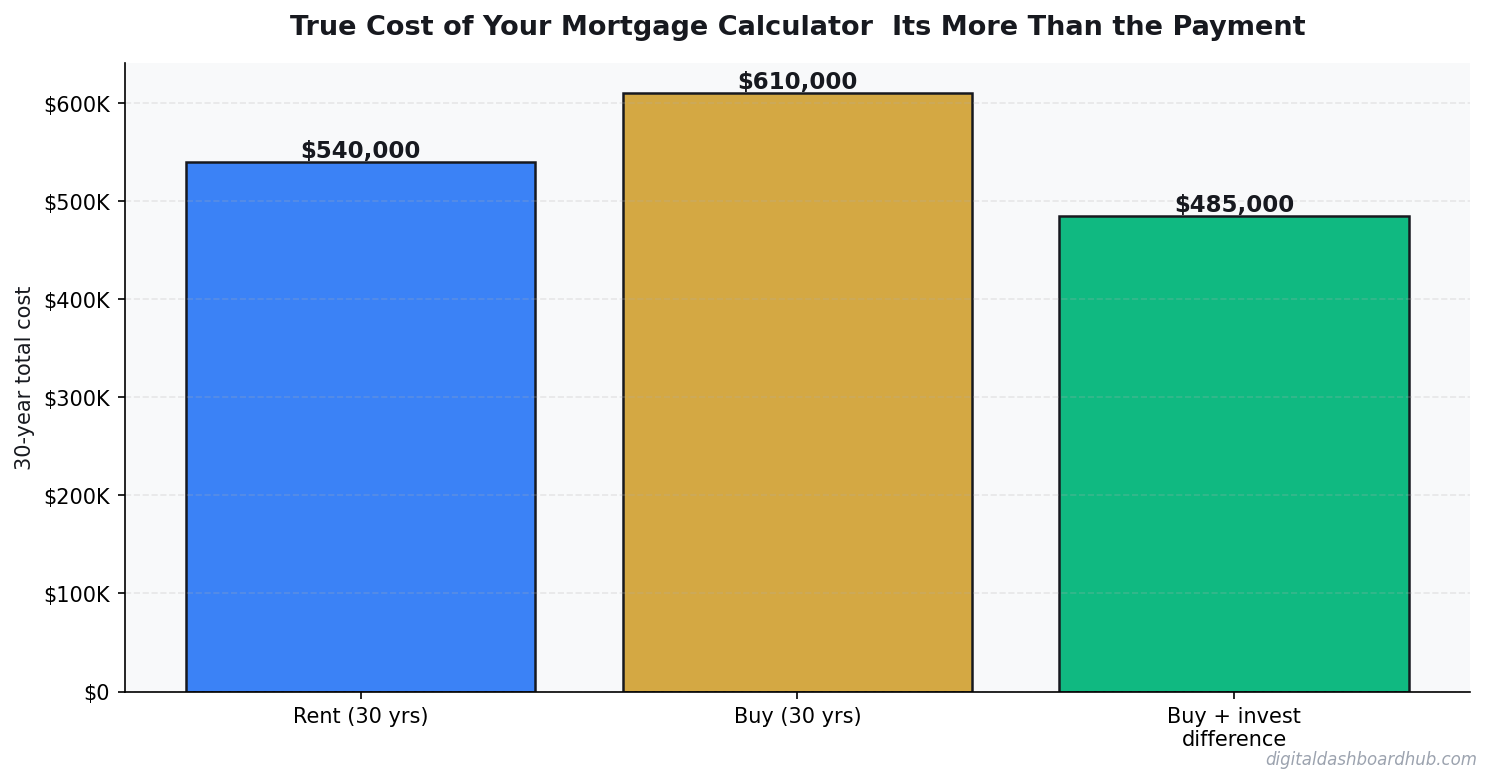

The Real Cost of a $350,000 Mortgage Over 30 Years

Here’s what almost nobody tells you at closing: a $350,000 mortgage at 7.1% over 30 years costs you $842,000 total. You’re paying $492,000 in interest — more than the home’s purchase price. Most buyers absorb this as a vague number. I want you to feel it concretely.

That $492,000 in interest would have grown to about $1.9M in a broad market index fund over 30 years at historical returns. That’s the true opportunity cost of the interest — not that homeownership is wrong, but that the “true cost” of a mortgage is far higher than the payment.

The Monthly Payment Is the Smallest Number You Should Care About

Lenders qualify you based on P&I. Buyers budget based on P&I. But your actual monthly housing cost is P&I plus property tax, insurance, PMI (if under 20% down), and HOA. On a $350K purchase with 10% down, those add-ons often total $700-$900/mo on top of the mortgage payment.

Practical example: $350K home, 10% down, 7.1% rate. P&I: $2,113/mo. Add taxes at $525/mo, insurance at $130/mo, PMI at $168/mo. Real monthly payment: $2,936 — nearly $800 more than the number in the lender’s headline rate quote.

The #1 Mistake Homebuyers Make With Mortgage Math

Optimizing for the lowest monthly payment instead of the lowest total cost. A 30-year mortgage at 7.1% has a lower payment than a 20-year at 6.8% — but costs you $211,000 more in total interest. If you can handle the payment, shortening the term is the highest-ROI financial move most homeowners never make. Even adding $200/mo to principal on a 30-year loan cuts 6-8 years and $90,000+ in interest.

Keep reading (related guides):

- Rental Property ROI Calculator: Is This Deal Actually Worth It?

- What Does a Wedding Actually Cost? 2026 Calculator With Real Data

- Wedding Budget Breakdown: Where Every Dollar Should Go (Free Calculator)

- Homeownership vs. Renting for 30 Years: The Complete Financial Comparison

- Bakery Revenue Calculator

255+ interactive tools for your money, time, and health.

Full features for 14 days · Secure payment · Stop anytime

Keep Reading

- Mortgage Comparison Calculator: Compare Rates

- Rent vs. Buy Calculator 2026

- How Sinking Funds Saved Me From Financial Emergencies

Common Questions About True Cost of Your Mortgage Calculator: It’s More Than the Payment

How long does it take to see results?

Most people see meaningful progress within 30-90 days when they apply these strategies consistently. The key is tracking your numbers from day one so you have a baseline to measure against.

What’s the biggest mistake people make?

Trying to do everything at once. Pick one or two strategies from this guide, implement them fully, then layer in additional tactics. Spreading yourself thin is the fastest way to see no results from any of it.

Do I need special tools or software?

Not necessarily to start — but the right tools eliminate hours of manual work. Our free calculators and trackers at Digital Dashboard Hub are a good starting point before you invest in paid software.

Andy Gaber is the founder of Digital Dashboard Hub, a suite of 255+ interactive financial, productivity, and wellness tools. He built DDH after getting frustrated with financial apps that gave outputs without context. Follow along for tool tutorials, revenue analytics breakdowns, and honest takes on personal finance.