Introduction: The Budgeting Method That Actually Feels Sustainable

You’ve probably heard it before: the moment you start budgeting, your life changes. But then reality hits—rigid budgets feel suffocating, tracking every penny feels like punishment, and most plans fall apart by February.

What if there was a budgeting approach that’s simple enough to teach a teenager, flexible enough to fit real life, and actually sustainable long-term?

50/30/20 Budget Calculator

Auto-split your income into needs, wants & savings with visual breakdowns and spending insights

Get the 50/30/20 Tool →

That’s where the 50/30/20 budget rule comes in. This framework has helped millions of people take control of their finances without turning budgeting into a second job. Whether you’re drowning in debt, struggling to save, or just tired of living paycheck-to-paycheck, this method might be exactly what you need.

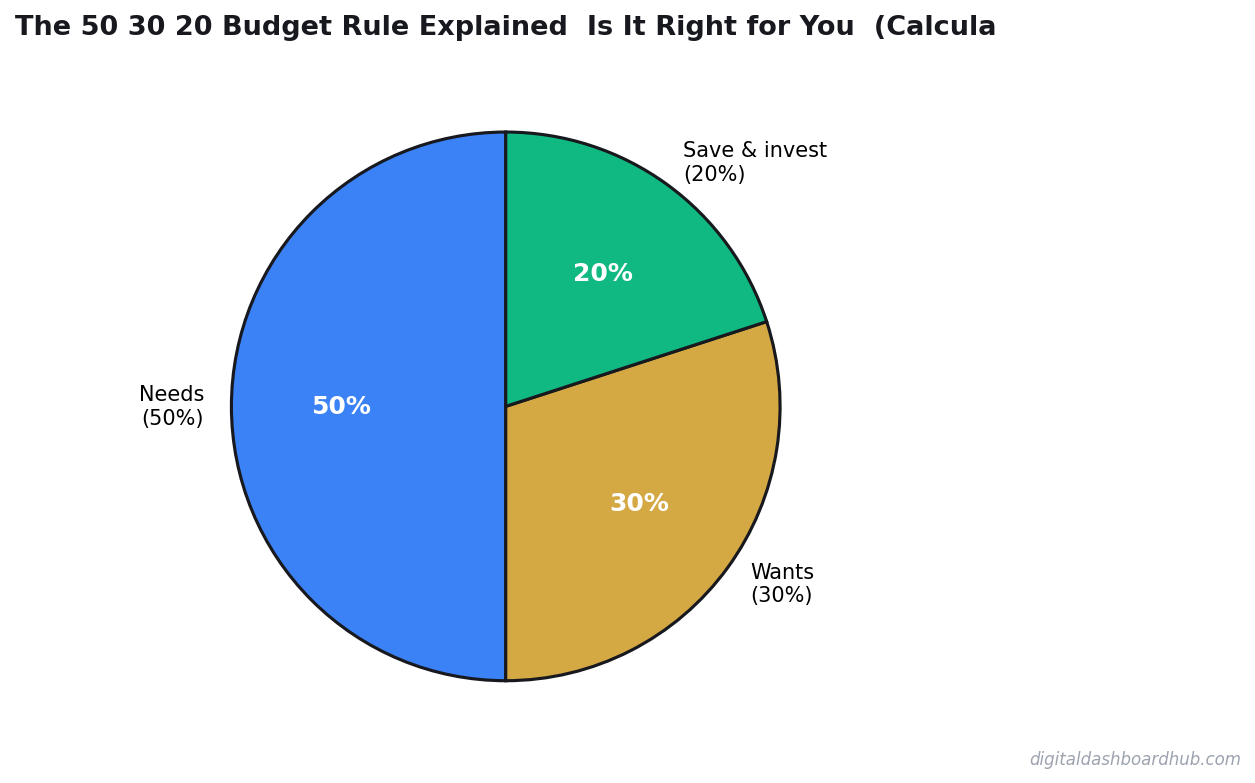

What Is the 50/30/20 Budget Rule?

The 50/30/20 rule is a simple budgeting framework that allocates your after-tax income into three categories:

- 50% for Needs — essentials you can’t live without

- 30% for Wants — things that improve your quality of life

- 20% for Savings & Debt Payoff — building your future financial security

This approach was popularized by Harvard bankruptcy researcher Elizabeth Warren in her 2005 book All Your Worth: The Ultimate Lifetime Money Plan, written with her daughter Amelia Warren Tyagi. The framework has remained relevant for two decades because it mirrors how successful people actually manage money—it’s balanced, realistic, and psychologically sustainable.

Breaking Down Each Category: Where Your Money Actually Goes

What Counts as “Needs” (50%)

Needs are non-negotiable expenses required for survival and basic functioning. These are the bills that show up regardless of how you feel that month.

Your needs typically include:

- Housing — rent or mortgage payments, property taxes, homeowners insurance, maintenance, utilities

- Food — groceries for home cooking (not restaurant meals)

- Transportation — car payment, insurance, gas, public transit, maintenance

- Insurance — health insurance, car insurance, renters insurance, life insurance

- Minimum debt payments — the mandatory minimum on credit cards, student loans, and other debts

- Basic utilities — electricity, water, internet, phone service

The 50% allocation for needs ensures that your essential expenses never spiral out of control. If your needs consistently exceed 50% of your income, you either need to find lower-cost housing, reduce transportation costs, or tackle the underlying income problem.

What Counts as “Wants” (30%)

Wants are everything that makes life enjoyable but isn’t strictly necessary. This is where budgeting gets fun—because yes, you should enjoy your life.

Your wants typically include:

- Dining out & takeout — restaurants, coffee shops, food delivery

- Entertainment — movies, concerts, streaming subscriptions, games

- Hobbies & shopping — clothes, books, sports equipment, personal items

- Vacation & travel — weekend trips, flights, hotels

- Subscriptions — gym memberships, apps, online services beyond basic internet

- Gifts — presents for friends and family

The 30% allocation gives you real breathing room to enjoy life without guilt. This is the budget category that makes the 50/30/20 rule so sustainable—you’re not white-knuckling your way through deprivation.

What Counts as “Savings & Debt Payoff” (20%)

Savings & debt payoff is your wealth-building category. This 20% goes toward securing your future and becoming financially independent.

This category includes:

- Emergency fund — building 3-6 months of expenses in savings

- Retirement contributions — 401(k), IRA, pension contributions

- Additional debt payments — paying extra toward high-interest debt

- Investments — stocks, bonds, real estate, other wealth-building vehicles

- Sinking funds — setting aside money for annual expenses like car registration or gifts

Many people skip this category thinking they’ll save “whatever’s left.” The 50/30/20 rule reverses that—you prioritize this 20%, and if money is tight, you adjust the other categories instead.

Real Examples: How 50/30/20 Works at Different Income Levels

Let’s see how this rule breaks down in real life across three income scenarios:

Example 1: $35,000 Annual Income (After-Tax Monthly: ~$2,330)

| Category | Percentage | Monthly Amount | Real Expenses |

|---|---|---|---|

| Needs (50%) | 50% | $1,165 | Rent ($700), utilities ($150), groceries ($200), car payment ($85), insurance ($30) |

| Wants (30%) | 30% | $699 | Dining out ($150), Netflix ($15), gym ($50), shopping ($200), coffee ($80), subscriptions ($100) |

| Savings (20%) | 20% | $466 | Emergency fund ($250), retirement ($150), extra debt payment ($66) |

At this income level, staying within the 50% needs allocation is challenging in high-cost areas. You might need to adjust to 60/25/15 and find ways to increase income.

Example 2: $55,000 Annual Income (After-Tax Monthly: ~$3,650)

| Category | Percentage | Monthly Amount | Real Expenses |

|---|---|---|---|

| Needs (50%) | 50% | $1,825 | Rent ($1,000), utilities ($180), groceries ($300), car payment ($200), insurance ($80), phone ($65) |

| Wants (30%) | 30% | $1,095 | Dining out ($250), entertainment ($100), hobbies ($200), shopping ($300), subscriptions ($150), travel fund ($95) |

| Savings (20%) | 20% | $730 | Emergency fund ($350), retirement ($250), extra debt payments ($130) |

At this income level, the 50/30/20 rule feels more natural and sustainable. You’re not stretched thin, and you have genuine room for enjoyment.

Example 3: $85,000 Annual Income (After-Tax Monthly: ~$5,660)

| Category | Percentage | Monthly Amount | Real Expenses |

|---|---|---|---|

| Needs (50%) | 50% | $2,830 | Mortgage ($1,400), utilities ($220), groceries ($400), car ($300), insurance ($200), childcare ($300) |

| Wants (30%) | 30% | $1,698 | Dining out ($400), entertainment ($250), hobbies ($300), shopping ($400), subscriptions ($200), travel ($150) |

| Savings (20%) | 20% | $1,132 | Emergency fund ($400), retirement ($500), extra debt payments ($200), investments ($32) |

At higher income levels, the 50/30/20 rule creates genuine wealth acceleration. The $1,132 monthly savings becomes $13,584 annually—real money that compounds into financial security.

Is the 50/30/20 Budget Rule Right for You?

Who Benefits Most from This Method

The 50/30/20 rule works exceptionally well for:

- Budgeting beginners who need a simple framework to start

- People with stable income who receive regular paychecks

- Those earning above median income in their area

- Individuals who want flexibility without micromanagement

- Anyone currently overspending on wants and needs

The beauty of this method is that it doesn’t require tracking every single transaction. You just need to know: what did I spend on needs, wants, and savings this month? Course-correct, and move forward.

Who Might Need to Modify This Rule

The 50/30/20 rule isn’t one-size-fits-all. You may need to customize it if you:

- Live in a high-cost area where housing eats 60%+ of income (adjust to 60/25/15 or 65/20/15)

- Carry significant debt and need to prioritize payoff (adjust to 50/30/20 with extra going to debt)

- Have an irregular income from freelancing or seasonal work (use average income and build larger emergency fund)

- Support dependents with disabilities or health issues (needs may legitimately exceed 50%)

- Earn very low income where basic needs exceed 50% (prioritize raising income alongside budgeting)

- Are in your peak saving years and want to accelerate wealth-building (adjust to 50/20/30 or even 50/15/35)

There’s nothing sacred about these exact percentages. They’re starting guidelines, not commandments.

How to Implement the 50/30/20 Budget in 5 Steps

Step 1: Calculate Your After-Tax Income

The 50/30/20 rule uses your after-tax monthly income. This is your actual take-home pay after federal, state, and payroll taxes are removed.

Find this by adding up all paychecks you receive in a month, or divide your annual after-tax income by 12. Don’t use gross income—it skews the percentages and sets you up for failure.

Step 2: Define Your Needs

Track every expense for one month and honestly categorize them. Look at your rent/mortgage, insurance, utilities, groceries, transportation, and minimum debt payments.

Add them up and divide by your after-tax income. If this exceeds 50%, you have a needs problem—not a willpower problem. Consider relocating, reducing transportation costs, or addressing income.

Step 3: Track Your Current Wants Spending

Many people are shocked when they actually track this category. That daily coffee, multiple subscriptions, and weekend shopping trips add up fast.

Look at your bank and credit card statements for 2-3 months. Categorize dining, entertainment, hobbies, shopping, and subscriptions. What’s the average monthly total?

Step 4: Define Your Savings Targets

Decide how you’ll allocate your 20%:

- How much goes to emergency fund (until you hit 3-6 months of expenses)?

- How much to retirement (aim for at least 15% of gross income)?

- How much to extra debt payments or investments?

Many people benefit from using separate bank accounts or automatic transfers to make this automatic and invisible.

Step 5: Adjust and Rebalance

If your percentages are way off (say, needs are 65% and wants are 20%), make a plan:

- For high needs: Find cost-cutting opportunities or increase income

- For high wants: Identify specific areas to reduce (usually subscriptions and dining are easiest)

- For low savings: Either cut wants or address needs—savings is where wealth is built

Review your budget monthly for the first three months, then quarterly after that.

Tools to Make 50/30/20 Budgeting Easier

While a simple spreadsheet works, dedicated budgeting tools help tremendously.

Our 50/30/20 Budget Calculator automates the math entirely—just enter your monthly income and watch it calculate exactly how much you can spend in each category. It’s perfect for quick budget reviews or teaching others about the rule.

If you prefer hands-on planning, our Monthly Budget Planner lets you track every month’s spending against your 50/30/20 targets. You’ll spot patterns quickly and know exactly which categories consistently exceed limits.

For those paid biweekly, the Biweekly Budget Template aligns perfectly with how you receive income—making it easier to assign paychecks directly to needs, wants, and savings.

If you’re attacking debt aggressively, the Paycheck Breakdown Analyzer helps you allocate every dollar strategically across categories, ensuring nothing gets missed or double-assigned.

For those who prefer cash, the Cash Envelope Budget brings the envelope method into the modern era—physical cash for wants keeps you aware of spending, while the tracker maintains overall 50/30/20 balance.

As you build your emergency fund, the Emergency Fund Calculator shows exactly how much you need and tracks progress toward your target.

Common Mistakes People Make with 50/30/20 Budgeting

Mistake 1: Including debt payments in wants. Extra debt payments go in the 20% savings category, not the 30% wants. Only minimum payments belong in needs.

Mistake 2: Using gross income instead of after-tax. Your actual paycheck is what matters. Using gross income inflates your budget and leads to consistent overspending.

Mistake 3: Never adjusting the percentages. Life changes. A job loss, child born, or move to an expensive area might require new percentages temporarily or permanently. That’s not failure—that’s adaptation.

Mistake 4: Forgetting annual and irregular expenses. Car registration, insurance premiums, holiday gifts, and medical deductibles aren’t monthly, but they still need to be budgeted. Divide annual costs by 12 and include them.

Mistake 5: Saving money “by accident.” If you’re hoping to save whatever’s left at month-end, you won’t. Treat the 20% as a bill you pay yourself first, automatically, before wants tempt you.

Customizing the 50/30/20 Rule for Your Situation

The original 50/30/20 splits work for many, but here are common customizations:

High-Cost-of-Living Areas: 60/25/15

If housing is 35% of income (instead of 25%), shift wants down to preserve some savings rate.

Aggressive Debt Payoff: 50/20/30

If you’re attacking student loans or credit cards, increase savings to 30% (focused on debt payoff) and trim wants to 20%.

High-Income Peak Years: 50/15/35

If you’re in your peak earning years (age 35-50), save aggressively. You’ll never regret overfunding retirement.

Very Low Income: 70/20/10

When basic needs genuinely require 70% of income, preserve 10% for emergency savings and work on increasing income. This is temporary, not permanent.

Single-Income Family: 50/25/25

Supporting dependents? A 25% wants budget (instead of 30%) combined with 25% savings (instead of 20%) creates better financial cushion.

The Psychology of the 50/30/20 Rule: Why It Actually Works

Here’s the real secret: the 50/30/20 rule works because it doesn’t require perfection.

Most budgeting methods fail because they demand superhuman discipline. But this rule works with human nature. You get to spend 30% guilt-free on things you genuinely enjoy. You’re not living on beans and rice forever. You’re not tracking every single transaction.

The framework gives you permission to enjoy life while building security. That psychological permission is what makes it sustainable for years, not weeks.

Research on financial behavior shows that people are more likely to stick with budgets when:

- The system is simple (three categories vs. twenty)

- There’s visible progress (watching the 20% grow compounds motivation)

- Some wants are allowed (not all pleasure is eliminated)

- The plan is flexible (percentages can shift as life changes)

The 50/30/20 rule hits all four of these points.

Final Thoughts: Starting Your 50/30/20 Journey

You don’t need a perfect budget to start building wealth. You need a simple, sustainable budget that you’ll actually follow for years.

The 50/30/20 rule has guided millions of people from financial stress to genuine security. It’s not because it’s complicated—it’s because it’s simple enough to stick with, flexible enough for real life, and effective enough to actually build wealth.

Start with your actual numbers this month. Calculate your after-tax income. Track where your money goes for one month. Divide into needs, wants, and savings. See where you stand.

If you’re at 55/30/15, you don’t need a revolution—you need a small adjustment. Cut $100 from wants and add it to savings. That’s it.

If you’re at 50/40/10, you have more work ahead, but it’s doable. Small monthly reductions to wants, combined with intentional savings, can reshape your financial life in 6-12 months.

The 50/30/20 rule works because you work. Your budget is just the map—you’re the one driving the car toward financial security.

Get Your Free 50/30/20 Budget Worksheet

Ready to implement the 50/30/20 rule? Download our free worksheet that walks you through calculating your exact allocation, tracking your categories, and customizing the percentages for your situation.

This worksheet is used by thousands of people who’ve successfully taken control of their finances using the 50/30/20 framework.

👉 Download the Free 50/30/20 Budget Worksheet — No spam, just the worksheet delivered straight to your inbox.

Keep reading (related guides):

- Free Sinking Fund Calculator — Try It Now

- Free Menopause Symptom Tracker — Try It Now

- Nervous System Regulation Tracker: The Visual Dashboard That Helps You Understand Your Bodys Stress Signals

- I Owed $47,000 in Taxes and Had $11,000 in the Bank: How I Rebuilt My Freelance Finances From the Ground Up

- Bakery Revenue Calculator

255+ interactive tools for your money, time, and health.

Full features for 14 days · Secure payment · Stop anytime

This article is for educational purposes only and shouldn’t be considered financial advice. Please consult a financial advisor for personalized guidance on your specific situation.

Disclaimer: This article is for informational purposes only and does not constitute professional advice. Always consult with a qualified professional for your specific situation.

Keep Reading

- I Tested 9 Expense Tracker Apps for 3 Months — Here’s What Actually Worked

- Freelancer Finance Management Dashboard (VVS): Finally, a Money Tool Built for Variable Income

- Airbnb Revenue Calculator: Estimate Your Short-Term Rental Income Before You List

Andy Gaber is the founder of Digital Dashboard Hub, a suite of 255+ interactive financial, productivity, and wellness tools. He built DDH after getting frustrated with financial apps that gave outputs without context. Follow along for tool tutorials, revenue analytics breakdowns, and honest takes on personal finance.