Someone told you “kids are expensive” and you nodded, but you’ve never actually run the numbers. That vague anxiety sitting in your stomach — the one that makes you wonder if you can actually afford to start a family — doesn’t go away until you replace “expensive” with a real dollar amount tailored to your life.

In This Article

The USDA Number Is Outdated — Here’s What’s Changed

Before you scroll: the calculator below is running in your browser right now. For the full feature set — saved scenarios, history, exports — open the dashboard.

I built Digital Dashboard Hub after spending years looking for tools that actually worked without a spreadsheet degree. Here’s what I’ve learned:

The USDA stopped updating their “Cost of Raising a Child” report after 2015. Since then, three cost categories have exploded:

Childcare: The average annual cost of center-based daycare hit $14,760 per year in 2025 (Child Care Aware of America). In cities like San Francisco, Boston, and DC, it regularly exceeds $25,000. That’s more than in-state college tuition at most public universities.

Housing: The median home price has jumped 38% since 2015. Families with children need, on average, one additional bedroom — and that bedroom costs $300-$800/month more depending on your market.

Healthcare: Adding a child to an employer health plan costs an average of $3,200/year in premium increases, plus out-of-pocket costs averaging $1,500/year for a healthy child (Kaiser Family Foundation, 2025).

Cost Breakdown by Category (Birth to 18)

Notice the range. The gap between a low-cost and high-cost approach is $452,400. That’s not a rounding error — it’s the difference between rural Alabama and downtown Manhattan, between public school and private, between hand-me-downs and Pottery Barn Kids.

The Costs Nobody Warns You About

Opportunity cost of lost income. If one parent reduces hours or leaves work for 3-5 years, the income loss (plus compounding career advancement) can exceed $200,000. This is the single largest “cost” of having a child, and it never appears in any calculator.

The “keeping up” tax. Birthday parties average $400-$500 each. Sports leagues run $500-$2,000/season. Summer camp ranges from $200/week (day camp) to $1,500/week (specialty overnight). None of these feel optional when your kid’s friends are all doing them.

Emergency buffer. Kids get sick. They break things. They need braces ($5,000-$7,000 average). The ER visit for the broken arm is $2,500 after insurance. Budget an extra $2,000-$3,000/year for the unexpected, or it comes out of your savings.

How the DDH Child Cost Calculator Handles This

Most online calculators give you a single national average number and call it a day. That’s not useful when you live in Portland, plan to use a nanny share instead of daycare, and know you’ll be paying for private school starting in middle school.

The DDH Child Cost Calculator lets you customize every major category by your actual situation. You select your metro area (or enter a custom cost-of-living adjustment), choose your childcare plan, toggle private vs. public school, and set your activity/extracurricular budget. The calculator then generates a year-by-year cost projection from birth through age 18.

When I ran my own numbers, the total came to $347,200 — about $50K less than the national average because I’m in a mid-cost city and plan to use public school. But the year-by-year view revealed something I hadn’t expected: ages 0-5 are the most expensive years, not the teenage years. Childcare alone accounted for 38% of my total cost in those first five years. That completely changed how I’m building my savings timeline.

Try the DDH Child Cost Calculator free — plug in your real numbers and get a personalized year-by-year projection.

FREE BONUS: The New Parent Financial Prep Checklist

27 financial tasks to complete before baby arrives, organized by trimester. Covers insurance, savings targets, budget adjustments, and legal documents.

Get instant access → Sign up free

How to Actually Afford It

The total number looks terrifying. But remember: you don’t pay $331K on Day 1. You pay it over 18 years — roughly $18,400/year on average, or $1,533/month. For context, that’s about what many people spend on a car payment plus insurance.

The key strategies that actually move the needle:

Front-load your savings for the childcare years. If daycare is $1,200/month for 5 years, start saving that amount 12-18 months before your due date. By the time the baby arrives, you’ll have a $14,400-$21,600 childcare fund that buys you breathing room during the most expensive phase.

Use a sinking fund strategy. Set up separate savings buckets for predictable big expenses: back-to-school ($500-$800/year), holiday gifts, summer camp, sports equipment. When the expense hits, the money is already there instead of coming from your checking account like a surprise.

Track the actual spend monthly. Most parents have no idea what they’re spending on their kids because it’s mixed into general household expenses. Separate it out. When you see that you spent $340 on kids’ clothing last month, you can make conscious choices about where that money goes.

Put This Into Action

Right now (5 minutes): Look at your last 3 months of bank statements and add up everything kid-related (or estimate what you’d spend). Compare that to the monthly averages in the table above. Are you above or below average for your region?

This week: Run your numbers through the DDH calculator with your actual city, childcare plan, and school preferences. The personalized number will either relieve your anxiety or give you a concrete savings target — both are better than guessing.

The long play:

Set up a dedicated “kid costs” sinking fund and automate monthly contributions. Even $200/month into a child expense fund for 12 months pre-baby gives you $2,400 in buffer before the first diaper.

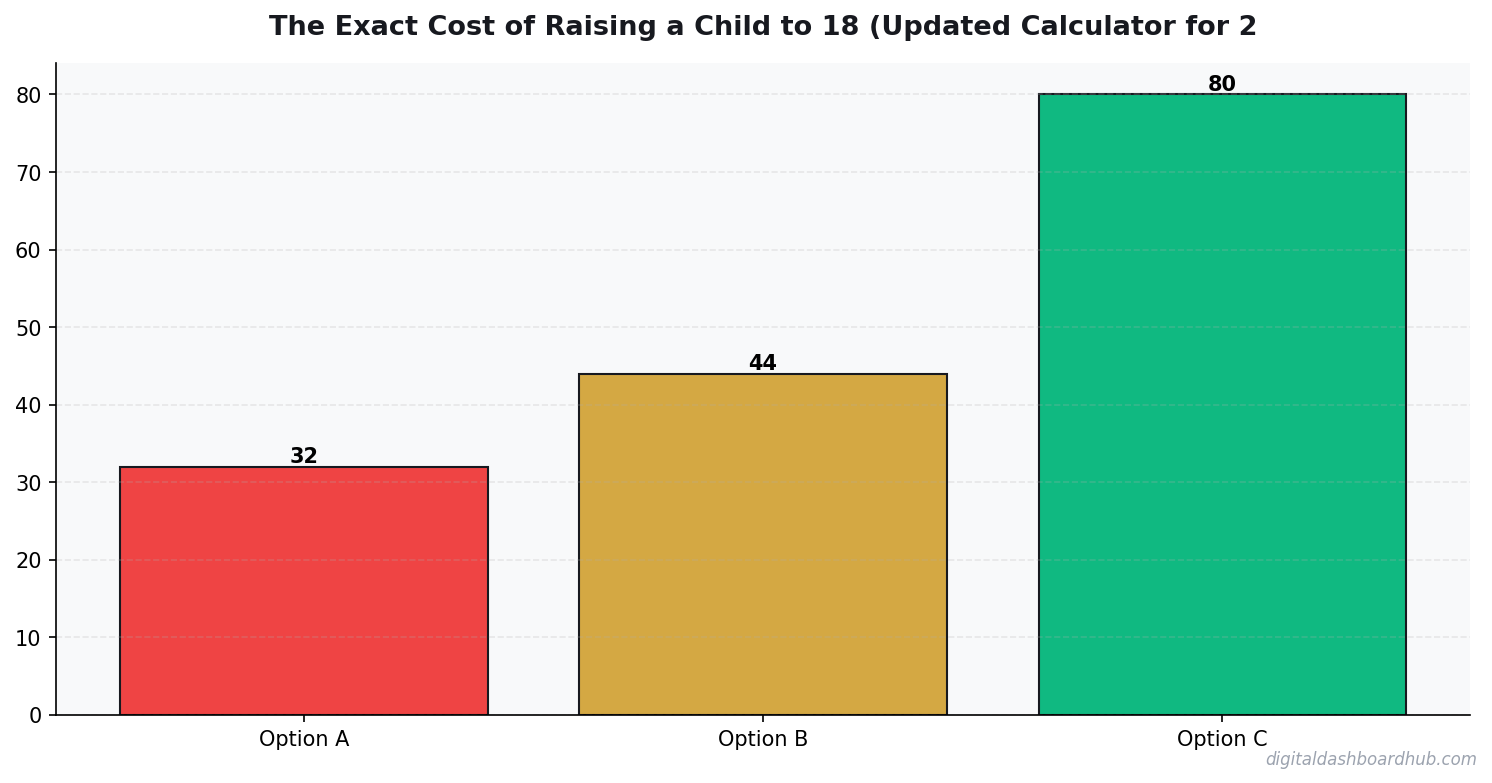

The Real Numbers: Raising a Child to 18 in 2026

The USDA’s often-cited figure (~$310,000) is a national average that obscures enormous geographic variation. Let me give you real numbers by cost tier.

Low-cost scenario (rural Midwest, state school): $180,000–$220,000 total to age 18. Housing cost delta is minimal in rural areas. Public school activities, local childcare, used vehicles — this is genuinely achievable.

National average (suburban, mixed public/private): $280,000–$340,000. Childcare alone from ages 0–5 runs $12,000–$18,000/year in most suburban markets — that’s $60,000–$90,000 before kindergarten. This number shocks most new parents because they didn’t budget for it before having children.

High-cost scenario (major metro, private school K-12): $500,000–$700,000 easily, not including college. Private school tuition in San Francisco, New York, or Boston runs $30,000–$50,000/year for K-12. That’s $390,000–$650,000 in tuition alone over 13 years.

The Category Most Parents Underestimate

Opportunity cost. When one parent reduces work hours or exits the workforce for childcare, the lifetime financial impact — lost wages, lost retirement contributions, lost Social Security credits, career trajectory disruption — often exceeds the direct cost of raising the child. A parent who works part-time from ages 32–40 may give up $300,000–$500,000 in lifetime earnings. That doesn’t make the choice wrong, but it belongs in the real cost calculation.

The most financially impactful decision most families make for child-cost management: childcare structure in years 0–5. High-quality subsidized childcare, shared childcare arrangements, or a family member providing care can save $50,000–$80,000 in that five-year window. It’s worth significant planning time before the child arrives.

The one expense category that surprises nearly every parent: childcare sick-day backup. When your child is too sick for daycare but you have work obligations, the backup options — in-home care, sick-day nanny services — cost $25–$45/hour with no notice. A family averaging one sick day backup per month pays $300–$540/year on top of regular childcare costs, often for a service they never budgeted for. Build a backup care budget line into your childcare planning — it will be used.

People Also Read

- Sinking Fund & Savings Goal Planner

- How Sinking Funds Saved Me From Financial Emergencies

- How to Use the 50/30/20 Budget Rule

- Emergency Fund 101: How Much You Really Need

Keep reading (related guides):

255+ interactive tools for your money, time, and health.

Full dashboard access · Stripe-secure checkout · Cancel anytime

Common Questions About Cost Raising Child Calculator 2026

How long before I see results?

Most people notice meaningful patterns within 2 to 4 weeks of consistent tracking. The first week is almost always noisy — you’re still learning what to record, when to record it, and how honest to be with yourself. By week two, baselines emerge. By week four, you can start testing changes against data instead of guessing. Don’t judge the system in the first seven days. Give it a full month before deciding whether the system is worth keeping or whether the approach needs a rethink.

What should I track first?

Start with one metric that is both objective and daily. Objective means a number, not a feeling. Daily means once every 24 hours, not “whenever I remember.” Two metrics is fine; three is too many to sustain for someone new. You can always add more once the habit is locked in. The goal of the first month is consistency, not coverage. It’s better to track one thing perfectly for thirty days than six things sloppily for five, and the data will be far more useful.

What if I miss a day?

Miss one day, no problem — tracking is a long game and single-day gaps don’t break the trend. Miss two days in a row, and your brain starts negotiating you out of the system entirely. The rule most people use: never miss twice. Log something — even a single data point — on the second day, then resume the full routine the next morning. Streaks matter less than quick recovery after a miss, and nobody maintains an unbroken record forever. The goal is resilience, not perfection.

Do I need a paid app to do this?

No. A notebook, a spreadsheet, or a free tool all work. The paid-app question should come after 4 weeks of consistent tracking, not before. If you’re going to quit inside the first two weeks, you’ll quit a free tool and a paid one at roughly the same rate. Prove the habit first, then decide whether a paid tool removes enough friction to be worth the subscription. Don’t use “finding the perfect app” as a way to avoid starting the system this week.

Andy Gaber is the founder of Digital Dashboard Hub, a suite of 255+ interactive financial, productivity, and wellness tools. He built DDH after getting frustrated with financial apps that gave outputs without context. Follow along for tool tutorials, revenue analytics breakdowns, and honest takes on personal finance.