Zero-Based vs. Traditional Budgeting: Why I Switched (And Never Went Back)

Scroll down — the interactive tool runs live with your inputs. Full version lives inside Digital Dashboard Hub. Two-click trial, Stripe-secure.

I’d been budgeting for three years and somehow still had no savings. Every month I’d open my banking app, see a number that felt too small, and wonder where the hell it all went. I wasn’t buying Ferraris — I was buying coffee, subscriptions, “just one more thing” at Target, and takeout because I was too tired to cook. Death by a thousand $14 charges.

In This Article

- Zero-Based vs. Traditional Budgeting: Why I Switched (And Never Went Back)

- Traditional Budgeting vs. Zero-Based: The Core Difference

- My Year in Numbers: Month-by-Month Breakdown

- The 5 Steps to Build Your First Zero-Based Budget

- How the DDH Budget Dashboard Handles This

- The Mindset Shift Nobody Talks About

- Common Objections to Zero-Based Budgeting

- Costly Mistakes I Made (So You Don’t Have To)

- Common Questions

- What I’d Do Differently If I Started Over

Then I discovered zero-based budgeting — the method where every single dollar gets assigned a job before the month starts, and your budget literally equals zero (income minus planned spending = $0). No “leftover” money sitting in checking, tempting you. Every dollar is spoken for. In my first year using this system, I saved $12,000 — more than I’d saved in the previous five years combined.

Traditional Budgeting vs. Zero-Based: The Core Difference

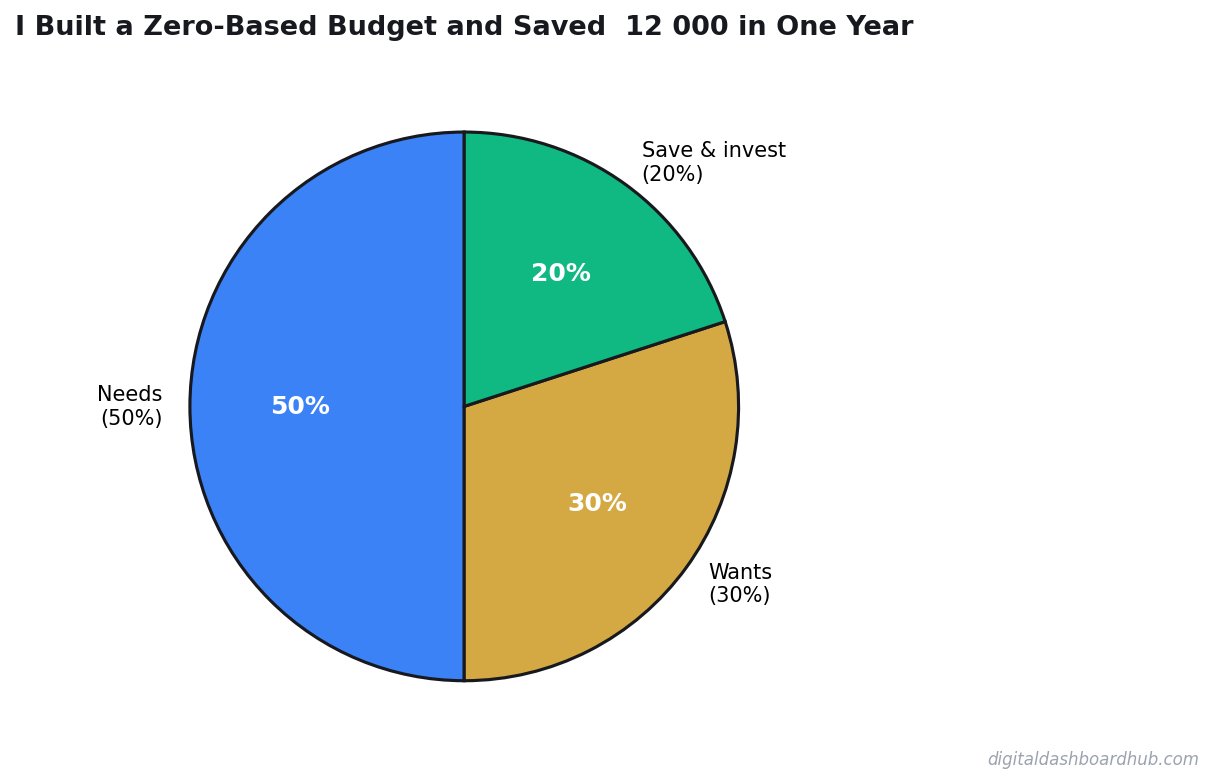

Most people budget like this: “I make $5,000. I’ll try to spend less than that.” Whatever’s left goes to savings. The problem? There’s never anything left. Spending expands to fill available money the same way work expands to fill available time.

Zero-based budgeting flips the equation. You start with your income, assign every dollar to a category — including savings, which gets treated as a “bill” — and your budget zeroes out. If you have $200 unassigned, you don’t leave it floating. You put it somewhere specific: extra debt payment, vacation fund, emergency savings.

The 50/30/20 rule is a fine starting point, but it lacks the granularity that catches the small leaks. Zero-based budgeting finds the $47 subscription you forgot about and the $180/month in “miscellaneous” that’s actually just impulse Amazon orders.

My Year in Numbers: Month-by-Month Breakdown

Here’s exactly what happened, with real numbers from my tracking data. My take-home pay averaged $4,800/month.

Months 1-3: The shock phase. I realized I’d been spending $340/month on subscriptions (Netflix, Spotify, gym I wasn’t using, two forgotten app trials, Amazon Prime, a meditation app I’d used twice). I cut $180 worth immediately. Savings those three months: $900, $1,100, $1,050.

Months 4-6: The optimization phase. Grocery spending dropped from $620 to $480 by meal planning on Sundays and actually sticking to a list. Takeout dropped from $380 to $180 — not zero, because I’m human, but halved by cooking batch meals twice a week. I also found $73/month in bank fees I could eliminate by switching to a no-fee checking account. Savings: $1,100, $1,200, $1,150.

Months 7-9: The autopilot phase. By now, the budget took 15 minutes per month to set up because I’d templated my categories. I was saving consistently without white-knuckling it. This is when the psychological shift happened — I stopped feeling like I was restricting myself and started feeling like I was choosing where my money went. Savings: $1,000, $1,050, $1,100.

Months 10-12: The acceleration phase. I got a small raise ($200/month after tax) and put all of it into savings instead of lifestyle inflation. I also sold some stuff I’d been meaning to get rid of, which added $800 over three months. Savings: $1,150, $1,200, $1,000.

Total saved: $12,000. Average $1,000/month on a $4,800 take-home. That’s a 20.8% savings rate — up from roughly 3% the year before.

The 5 Steps to Build Your First Zero-Based Budget

Step 1: Calculate your actual take-home pay. Not your salary — your take-home. After taxes, insurance, and 401k contributions. If your income varies (freelancers, contractors), use your lowest month from the past 6 months as your baseline. Variable income budgeting has its own rules.

Step 2: List every fixed expense. Rent/mortgage, car payment, insurance, minimum debt payments, phone bill. These are non-negotiable and don’t change month to month. For me, this totaled $2,340.

Step 3: Set your savings target as a “bill.” This is the key insight of zero-based budgeting — savings isn’t what’s left over, it’s a fixed expense. I started with $500/month and worked up to $1,000. Put it right after rent in your budget, before groceries or entertainment.

Step 4: Allocate remaining dollars to variable categories. Groceries, gas, entertainment, personal care, clothing, gifts. Every dollar gets assigned. If you have $50 left after everything is assigned, don’t leave it — put it toward your highest-priority goal (debt payoff, emergency fund, or a sinking fund).

Step 5: Track daily and adjust weekly. The budget is a plan. Reality is messy. When you overspend on groceries, you pull from entertainment — not from savings. The zero-based system forces you to make trade-offs in real time rather than discovering overages after the fact.

FREE BONUS: The Zero-Based Budget Starter Template

Pre-built spreadsheet with income, fixed expenses, savings, and variable categories. Includes a monthly review checklist and category suggestions based on average American spending data.

Get instant access → DOWNLOAD FREE

How the DDH Budget Dashboard Handles This

I built my first zero-based budget in a spreadsheet. It worked, but it was clunky. The DDH Budget Dashboard was built specifically for this method.

You enter your take-home pay, and it walks you through assigning every dollar — fixed expenses first, then savings (treated as a “bill”), then variable categories. The running balance meter at the top shows your unassigned dollars counting down to zero in real time. It’s oddly satisfying to watch it hit $0.

Daily tracking happens through quick category entries. Spent $47 on groceries? Tap the category, enter the amount. The dashboard updates your remaining budget for that category instantly and shows you the pace indicator — are you spending faster or slower than your daily rate for this category? If it’s day 15 and you’ve used 70% of your grocery budget, the indicator flags yellow.

The monthly rollover feature is what separates it from most budget apps. Zero-based purists reset every month. But real life doesn’t reset — if you underspent on clothing by $50, the DDH dashboard lets you roll that $50 into next month’s savings or redirect it to a sinking fund. Flexible enough to be realistic, structured enough to keep you honest.

→ Try the DDH Budget Dashboard free: app.digitaldashboardhub.com/signup

The Mindset Shift Nobody Talks About

What changed everything surprised me more than the $12,000: I stopped feeling broke. Before zero-based budgeting, I technically had more “available” money because nothing was allocated. But that money felt precarious because I knew it could disappear at any moment — and it usually did.

After zero-based budgeting, I had less “available” money because every dollar was assigned. But I felt financially secure for the first time in my adult life. I knew exactly where my money was going. I had an emergency fund growing. I had sinking funds for car repairs and holiday gifts. The next unexpected expense wasn’t going to wreck me.

A 2024 Bankrate survey found that 56% of Americans can’t cover a $1,000 emergency expense from savings. After 6 months of zero-based budgeting, I had $6,000 in an emergency fund. Not because I made more money — because I told my existing money where to go instead of wondering where it went.

Common Objections to Zero-Based Budgeting

“It takes too much time.” The first month takes 30-45 minutes to set up. After that, it’s 15-20 minutes per month because your categories are templated. Daily tracking takes under 2 minutes. Compare that to the hours you spend worrying about money.

“My income is irregular.” Zero-based budgeting actually works better for variable income than traditional budgeting. Budget your lowest expected month. When you earn more, the excess goes to a buffer fund that smooths out lean months. It’s how every freelancer I know who’s good with money operates.

“I don’t want to restrict myself.” Zero-based budgeting isn’t about restriction — it’s about intention. You can budget $200 for entertainment. You can budget $100 for coffee. The point isn’t to spend less on everything; it’s to spend intentionally on what matters and cut the spending that doesn’t.

“What about unexpected expenses?” That’s what sinking funds are for. I budget $100/month for car maintenance, $50/month for medical copays, $75/month for home repairs. When those expenses hit, they’re already funded. They stop being “emergencies” and start being “expected costs.”

Costly Mistakes I Made (So You Don’t Have To)

Financial tracking seems straightforward until you actually do it. Here’s where I went wrong.

Common Questions

How much should I save each month?

The 50/30/20 rule is a starting point, but it doesn’t work for everyone. I track actual spending for 30 days first, then set realistic targets. Most people who jump straight to aggressive saving goals quit within 6 weeks.

What’s the easiest budgeting method for beginners?

Zero-based budgeting sounds intimidating but it’s actually the simplest once you set it up. Every dollar gets assigned a job before the month starts. I spent 45 minutes setting mine up and it runs on autopilot now with weekly 5-minute check-ins.

How do I budget with irregular income?

Base your budget on your lowest-earning month from the past 6 months. Anything above that goes into a buffer fund. I freelanced for 3 years and this method eliminated the feast-or-famine stress completely.

What I’d Do Differently If I Started Over

Start with tracking, not budgeting. I jumped straight into a zero-based budget without knowing where my money was actually going. Spend 30 days just tracking every expense — no judgment, no changes. Then build your budget around reality, not aspirations. Most people underestimate their food spending by 40-60%.

Build the emergency fund BEFORE aggressive saving. I tried to save $1,000/month from day one and depleted my checking account to dangerously low levels twice. Start with $500 in an emergency buffer, then ramp up.

Use a dedicated tool, not a generic spreadsheet. My spreadsheet had 14 tabs by month 6 and I dreaded opening it. A purpose-built budget tracker with auto-calculations would have saved me hours.

Make It Happen

1. Right now (2 minutes): Open your bank app. Look at last month’s transactions. Find one subscription you forgot about or no longer use. Cancel it. That’s your first zero-based budget win.

2. This week: Write down your take-home pay. List your fixed expenses. Subtract. That remaining number is what you have to divide between savings and variable spending. Even this rough sketch is more clarity than most people ever get.

3. The long game: Build your first full zero-based budget using the DDH Budget Dashboard. Assign every dollar. Track daily for one month. The average DDH user finds $180/month in “invisible” spending they can redirect to savings.

Still here? You’re serious about this.

Join 700+ people who downloaded the Zero-Based Budget Starter Template this month. Most people find at least $150 in spending they can redirect within the first week.

Get your free copy → DOWNLOAD FREE

Keep reading (related guides):

- Business Expense Tracker: Categorize and Export for Tax Time

- How Much Money You Need to Retire Early at 40, 45, and 50 (Real Numbers by Age)

- Youre Probably Wasting $200/Month on Subscriptions You Forgot About (Heres How to Find Them)

- Free ADHD Impulse Spending Tracker — Try It Now

- Small Business Finance Basics: The Only 5 Numbers You Need to Track Weekly

255+ interactive tools for your money, time, and health.

14 days free · No charge today · 2-click cancel

What Changed After 90 Days of Tracking

The first month of tracking zero based budget saved 12000 one year was frustrating. The data looked random, the patterns weren’t obvious, and I questioned whether logging this stuff daily was worth the 3 minutes it took.

The second month was when patterns started emerging that I couldn’t see in week-to-week data. A specific correlation appeared between my weekend habits and Monday results — the kind of insight that only surfaces with enough historical data points.

By month 3, I was making decisions ba

sed on data instead of gut feelings. My results improved not because I worked harder, but because I stopped doing the things the data showed weren’t working. That’s the real value of tracking — it’s not about motivation, it’s about information. You can’t optimize what you don’t measure, and you can’t measure what you don’t track consistently.

You Might Also Like

- Zero-Based Budgeting: How to Give Every Dollar a Job

- How to Save $10,000 in 6 Months: A Realistic Plan

- I Tested 9 Expense Tracker Apps — My testing revealed Actually Worked

- Savings Rate Calculator: The One Number That Predicts Your Financial Future

Andy Gaber is the founder of Digital Dashboard Hub, a suite of 255+ interactive financial, productivity, and wellness tools. He built DDH after getting frustrated with financial apps that gave outputs without context. Follow along for tool tutorials, revenue analytics breakdowns, and honest takes on personal finance.