You’ve done the math on retiring at 65. That number probably doesn’t excite you. What if you started running the numbers for 40? Or 50?

This guide breaks down the retire early money needed by age — 40, 45, and 50 — with real numbers, not vague ranges. Then shows you how to calculate your specific number based on what you actually spend.

Why Retirement Age Changes Everything

Before DDH, I was doing this manually in spreadsheets. Here’s the faster way:

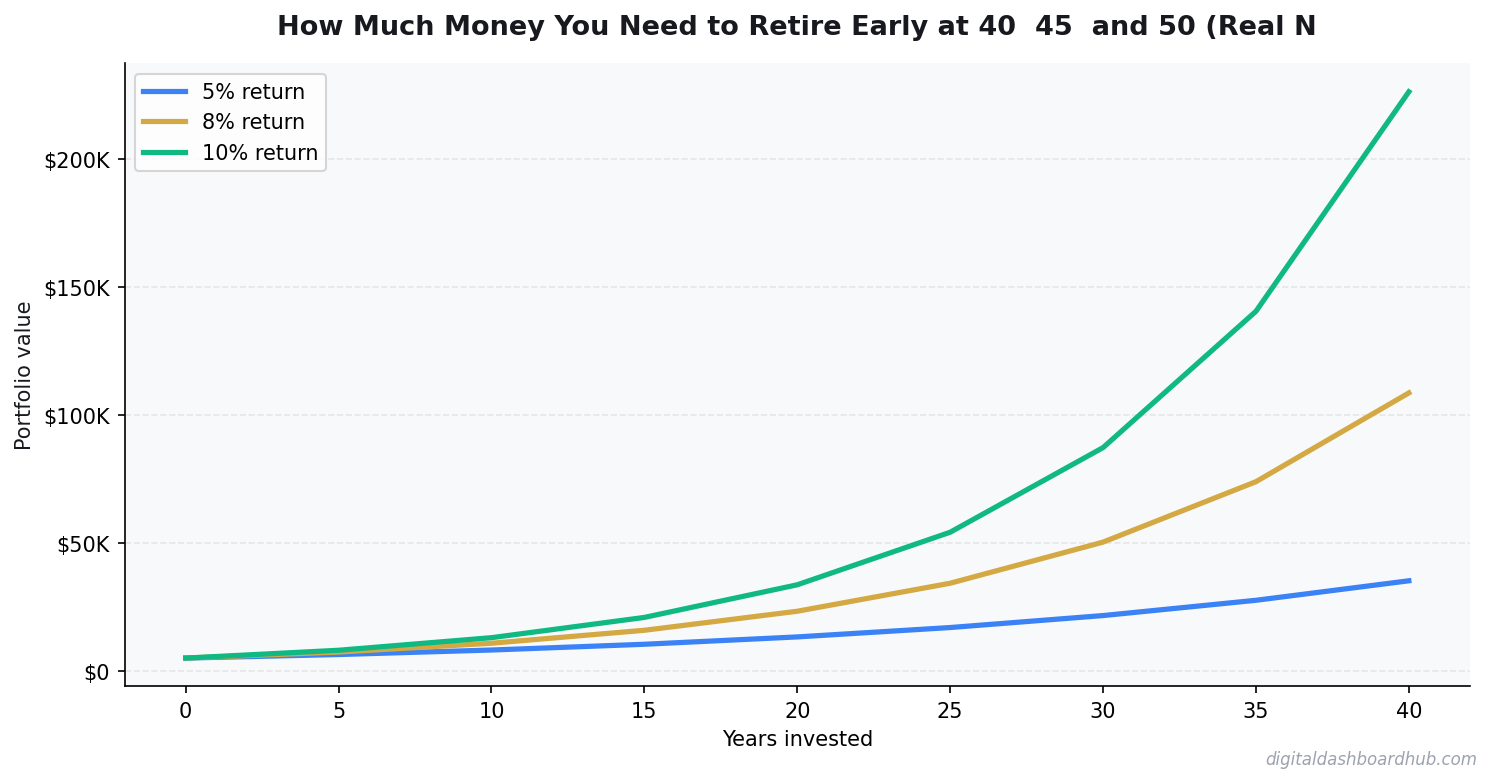

Here’s what most people miss: the problem with retiring early isn’t just saving more money. It’s that your money needs to last longer.

Retire at 65 and your portfolio needs to cover 25–30 years. Retire at 45 and it needs to cover 40–50 years. That changes the math significantly.

The standard “4% rule” (withdraw 4% of your portfolio annually, adjusted for inflation, and it lasts 30 years) starts to strain past 30 years. Many early retirement researchers recommend a 3.5% or even 3.25% withdrawal rate for retirements expected to last 40+ years.

This is the most important variable in early retirement math, and most calculators ignore it.

Step 1: Calculate Your Annual Spending (Not Your Income)

Most people track their income. Very few track their actual spending. Your retirement number is based on spending — and if you don’t know what you spend, any projection is fiction.

Here’s how to find your real number in 20 minutes:

- Download 12 months of bank and credit card statements

- Add up every dollar spent (exclude income taxes — those change dramatically in retirement)

- Subtract work-related expenses: commuting, work clothes, convenience food you buy because you’re busy

- Add back in what you’d spend more of in retirement: travel, hobbies, healthcare before Medicare eligibility

Most people find their retirement spending is 15–25% lower than their working-life spending once you strip out work-related costs. Some find it’s higher because they plan to travel more.

Whatever number you land on — that’s your annual retirement spending. Write it down. Everything else is math.

Step 2: The Right Withdrawal Rate by Age

| Retirement Age | Expected Duration | Recommended Withdrawal Rate |

|---|---|---|

| 65 | 25–30 years | 4.0% |

| 60 | 30–35 years | 3.75% |

| 55 | 35–40 years | 3.5% |

| 50 | 40–45 years | 3.25% |

| 45 | 45–50 years | 3.0% |

| 40 | 50+ years | 2.75–3.0% |

These rates are based on historical simulations using US stock market data (90%+ success rate over the specified periods). Your actual safe withdrawal rate depends on your asset allocation, expected healthcare costs, and whether you have any guaranteed income.

Step 3: The Early Retirement Number by Age

Now plug in your annual spending. I’ll use $60,000/year as the example — a common figure for a frugal but comfortable lifestyle.

Retire at 40 — Your FIRE Number

Using a 2.75% withdrawal rate (conservative for a 50+ year horizon):

$60,000 ÷ 0.0275 = $2,181,818

Call it $2.2 million. That’s the target if you’re retiring at 40 with zero guaranteed income and want 95%+ confidence your portfolio survives to age 95.

Retire at 45 — Your FIRE Number

Using a 3.0% withdrawal rate:

$60,000 ÷ 0.030 = $2,000,000

$2 million. The additional 5 years of working (vs. retiring at 40) reduces your required portfolio by roughly $180,000 — and gives you 5 more years of compounding and contributions. For many people, retiring at 45 instead of 40 is significantly more achievable with the same lifestyle.

FREE BONUS: The FIRE Number Tracker (Google Sheet)

Pre-built spreadsheet that tracks your progress toward your FIRE number — shows your gap, timeline, and monthly savings target.

Get instant access → app.digitaldashboardhub.com/signup

Retire at 50 — Your FIRE Number

Using a 3.25% withdrawal rate:

$60,000 ÷ 0.0325 = $1,846,154

~$1.85 million. Retiring at 50 also unlocks some advantages: you’re closer to Social Security eligibility, and healthcare costs are 12 years shorter before Medicare kicks in at 65. The 50-year-old FIRE number is often the most achievable sweet spot for people who started their financial independence journey in their 30s.

How Your Spending Changes the Numbers

| Annual Spending | Retire at 40 | Retire at 45 | Retire at 50 |

|---|---|---|---|

| $40,000/year | $1.45M | $1.33M | $1.23M |

| $60,000/year | $2.18M | $2.00M | $1.85M |

| $80,000/year | $2.91M | $2.67M | $2.46M |

| $100,000/year | $3.64M | $3.33M | $3.08M |

The single most powerful lever in early retirement isn’t your investment return — it’s your spending. Reducing annual expenses by $20,000 cuts your required portfolio by $700K+ at a 3% withdrawal rate. That’s years off your timeline.

Step 4: How Many Years Does It Take to Get There?

Here’s where the DDH Retire Early calculator earns its keep. Enter your current savings, monthly contribution, expected return, and target FIRE number — and it shows your projected retirement date.

A 35-year-old with $200,000 saved, adding $3,000/month to investments earning 7% annually, targeting a $2M FIRE number:

- Projected date: 13.4 years from now — retire at 48

- Portfolio at 60: $7.2M (assuming continued growth at conservative 5%)

- Monthly income at 3.25% SWR: $5,850

That’s achievable. And it’s specific. Not “invest more and retire rich someday” — but 13.4 years, a concrete number, and a monthly income projection.

→ Run your own numbers: app.digitaldashboardhub.com/signup

The Variables That Change Everything

Healthcare Before 65

This is the #1 overlooked cost in early retirement planning. Without employer coverage, a 45-year-old couple buying ACA marketplace insurance can expect $1,200–2,000/month in premiums alone. That’s $14,400–24,000/year not in your spending estimate.

The fix: Add your expected healthcare costs explicitly to your annual spending figure before calculating your FIRE number. The DDH calculator has a healthcare cost field for exactly this reason.

Social Security

If you retire early, you’re not collecting Social Security at 62 — you’re waiting. And every year you delay past 62 (up to 70) increases your benefit by roughly 8%.

But here’s the nuance: your benefit is based on your 35 highest-earning years. If you retire at 45 with 20 years of work history, your benefit will be calculated using 15 zero-earning years in the formula. Model your actual projected benefit at ssa.gov/myaccount. It takes 5 minutes. Then factor that guaranteed income into your FIRE number.

Part-Time Income in Early Retirement

Many early retirees find they don’t fully stop working — they just stop working jobs they hate. Consulting 10 hours/week, a small business, rental income, or monetized hobbies can add $1,000–3,000/month.

Every dollar of reliable part-time income reduces your FIRE number by $30–36 at a 3% SWR. If you can generate $2,000/month in flexible income, your required portfolio drops by $600,000–720,000.

How the DDH Retire Early Calculator Handles This

The calculator models your full financial picture.

Input: Current age, current savings, monthly contributions, expected investment return, annual spending, Social Security estimate (optional), and any expected part-time income.

Output: Your projected FIRE date, your FIRE number, a year-by-year portfolio projection, your safe withdrawal amount, and a sensitivity analysis showing how a 1% return change or $500/month spending change affects your timeline.

Most users find their FIRE date is within 10–15 years — which shifts the conversation from “someday” to “actually possible.”

The Objections Worth Addressing

“What if the market tanks right after I retire?” This is the “sequence of returns” risk — and it’s real. The approach is a cash buffer (1–2 years of expenses in cash/stable assets) and a flexible withdrawal strategy (spending less in down years).

“What about inflation?” The FIRE numbers above assume a 3–3.5% long-term inflation rate baked into the withdrawal rate math. The 4% rule and its variants are already inflation-adjusted over historical periods.

“I can’t save that much.” The most direct path to a lower FIRE number is lower spending, not higher income. A lifestyle costing $40,000/year reaches financial independence with $600,000 less needed than one costing $60,000/year.

Your Next Move

1. Right now (20 minutes): Pull 12 months of actual spending from your bank and card statements. Find your real annual spending number.

2. This week: Enter your numbers into the DDH Retire Early calculator. Find your FIRE number, your projected date, and the one lever that moves your timeline the most.

3. Long game: Track net worth monthly in the DDH dashboard. Watching your FIRE gap close — even by $500/month — is one of the most motivating financial experiences you can have.

Still here? You’re already ahead of most people.

Most people think about early retirement. You’re calculating it. Get the FIRE Number Tracker and the full DDH suite — free for 14 days.

Start tracking → app.digitaldashboardhub.com/signup

Keep reading (related guides):

- Never Work Again Calculator: The Exact Number by Age

- The Exact Number You Need to Never Work Again — By Age (How to Calculate It)

- How to Calculate Your Net Worth (And Why Its the Only Financial Number That Matters)

- Investing for Beginners: How to Start With Just $50 (And Actually Understand What Youre Doing)

- Free Sinking Fund Calculator — Try It Now

255+ interactive tools for your money, time, and health.

Full dashboard access · Stripe-secure checkout · Cancel anytime

Keep Reading

- How Much Do I Need to Retire? A Simple Framework

- Sinking Fund & Savings Goal Planner: The Free Visual Dashboard

- How Sinking Funds Saved Me From Financial Emergencies

Andy Gaber is the founder of Digital Dashboard Hub, a suite of 255+ interactive financial, productivity, and wellness tools. He built DDH after getting frustrated with financial apps that gave outputs without context. Follow along for tool tutorials, revenue analytics breakdowns, and honest takes on personal finance.