Introduction: Breaking Through the Investing Barrier

If you’ve ever thought about investing but felt like you needed a fortune to start, this article is for you. The biggest myth about investing? You need a lot of money to begin. The truth is simpler: you need clarity, a system, and a willingness to start small.

Investing isn’t magic. It’s not rocket science. And you don’t need to understand every technical detail to get started and watch your money grow. Thousands of beginners start with $50 or less every month and build real wealth over time.

The challenge isn’t money—it’s understanding what you’re actually doing. That’s what we’re fixing today.

Part 1: Demystifying the Core Concepts

What Actually Happens When You Invest?

Investing means putting your money into assets—like stocks, bonds, or funds—that can grow over time. Instead of your money sitting in a savings account earning almost nothing, it works harder.

Here’s the simple version:

Stocks = Tiny pieces of ownership in companies. When you buy a stock, you own a small slice of that business. If the company does well, your slice becomes more valuable.

Bonds = IOUs from companies or governments. You lend them money, they promise to pay you back with interest. Less exciting than stocks, but more stable.

ETFs (Exchange-Traded Funds) = Baskets of stocks or bonds bundled together. Instead of picking individual stocks (which requires research), you buy one ETF that might contain 500 different companies. This spreads your risk.

Index Funds = A type of ETF that tracks an entire market index, like the S&P 500 (500 large companies) or the NASDAQ (tech-heavy companies). You’re essentially betting on the entire market, not picking winners.

The Secret Weapon: Compound Interest

This is where investing gets powerful.

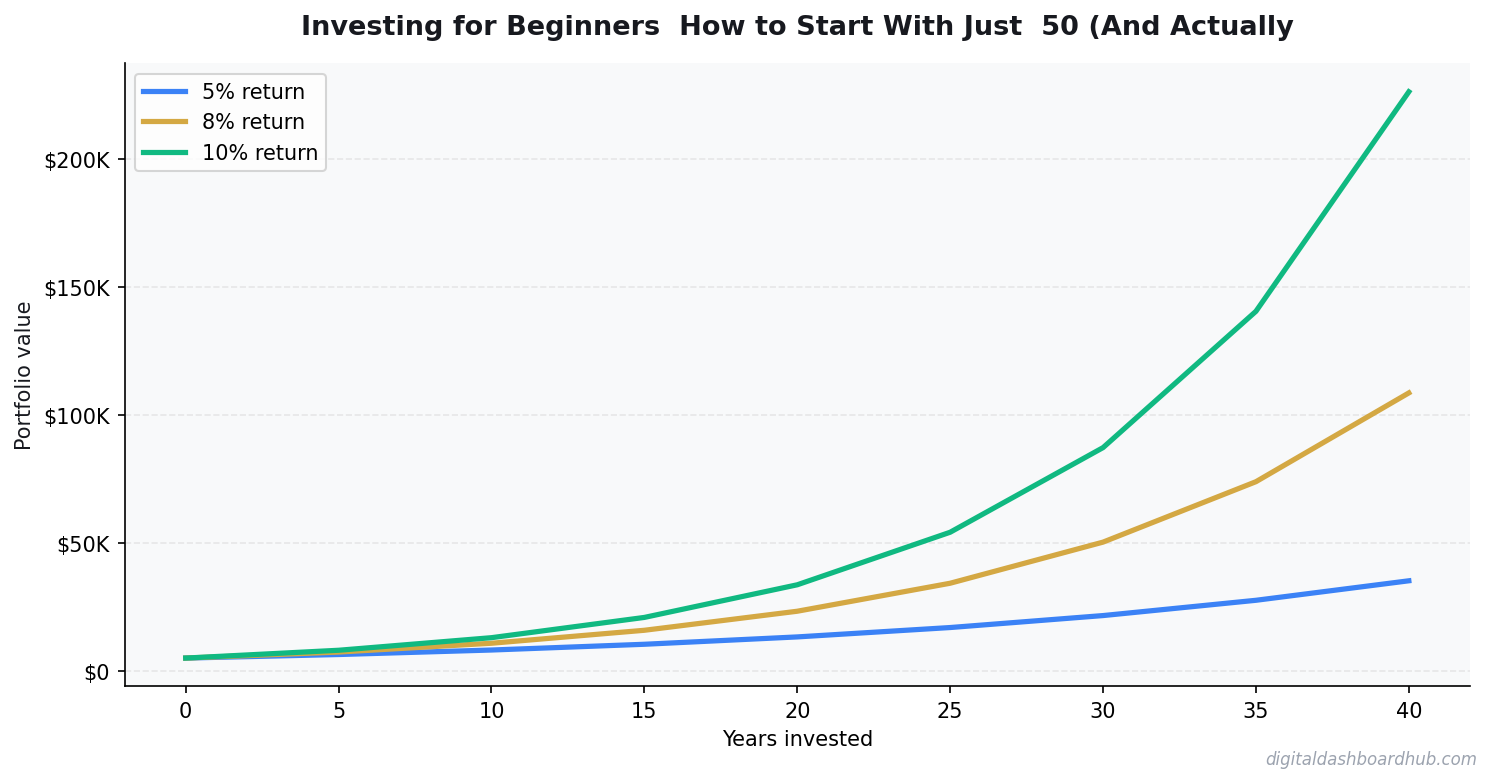

Albert Einstein supposedly called compound interest the “eighth wonder of the world.” Here’s why: your money doesn’t just grow on what you invest. It grows on the growth itself.

Let’s use real numbers:

- Your contributions: $18,000 (that’s just $50 × 12 months × 30 years)

- Your account value at the end: ~$79,000

Your money more than quadrupled without you doing anything special. That extra $61,000 came from compound growth. Your original money earned returns, then those returns earned returns, and so on for three decades.

Start earlier, and the numbers get even more dramatic. Start at 25 instead of 35, and you’re looking at $300,000+ from those same $50 monthly contributions.

This is why patience is an investment superpower.

Part 2: Starting Small—Yes, $50 Is Enough

| Option | Cost | Time Investment | Customizable? | Best For |

|---|---|---|---|---|

| DIY approach | Free | High | Fully | Those with time to build from scratch |

| Generic tool | $5-$50/mo | Medium | Limited | Standard use cases |

| DDH Free Tool | Free trial | 5-10 min setup | Yes | Getting real answers without spreadsheet hell |

How Fractional Shares Changed Everything

Ten years ago, you needed $150+ just to buy a single share of certain companies. Many beginners were locked out before they started.

Today? Fractional shares. Apps like Fidelity, Vanguard, Charles Schwab, and others let you buy tiny pieces of stocks or ETFs with any dollar amount. You can invest $5, $25, or $50—whatever you have—and own a proportional piece.

The Micro-Investing Apps

These apps are designed specifically for beginners:

- Acorns or Digit: “Round up” your everyday purchases. Buy coffee for $4.50? They round it to $5 and invest the $0.50. It adds up surprisingly fast.

- Betterment: Automated investing with a low minimum. Answer a few questions about your risk tolerance, and it builds a custom portfolio for you.

- Robinhood or Fidelity: Zero fees, fractional shares, and low or no minimums.

The barrier to entry isn’t money anymore. It’s deciding to start.

Building Your First Portfolio at $50

Here’s what a simple beginner portfolio might look like with $50:

- $35 in a low-cost S&P 500 index fund (VTI, VOO, or similar) — this gives you exposure to 500 large U.S. companies

- $15 in an international stock index fund (VXUS or similar) — diversification across the globe

That’s it. Two funds. One investment gives you broad U.S. exposure; the other gives you global exposure. You’re immediately diversified beyond what most millionaires had 30 years ago.

Part 3: What to Track As a New Investor

Knowing what to measure keeps you focused and prevents emotional decision-making.

1. Portfolio Value

Track your total account balance monthly. Not daily—daily fluctuations will drive you crazy. Monthly is enough to see trends without noise.

Use a simple spreadsheet or a tracker. Our Net Worth Tracker and Dashboard Assets template is designed exactly for this, giving you a clear visual of growth over time.

2. Asset Allocation

Know what you own. If your plan is 80% stocks and 20% bonds, check quarterly to make sure you’re still at that ratio. Market moves will push these around.

Example: After a strong year, your stocks are now 85% of your portfolio. A quarterly rebalance brings it back to 80%.

3. Total Contributions vs. Growth

Separate the money you put in from the money your money earned. This shows you the real power of compound growth.

After one year: $600 invested, $37 earned = $637 total. You can literally see your money working.

4. Fees

This matters more than beginners realize. A fund charging 1% annually sounds small. Over 30 years, it compounds against you. The difference between a 0.1% fee fund and a 1% fee fund? Around $100,000+ on a $500,000 portfolio.

Always check the expense ratio (ER) of any fund you buy. Aim for under 0.20%.

5. Performance vs. Benchmarks

Compare your returns to relevant benchmarks. If you’re invested in U.S. stocks, compare to the S&P 500. If international, compare to the MSCI World index.

You don’t need to beat the market—just match it. If you’re keeping up with your benchmark, you’re winning.

Part 4: The Beginner Mistakes That Cost Real Money

Mistake #1: Timing the Market

You hear about the stock market dropping and think, “I’ll wait until it recovers to invest.”

Here’s what actually happens: The market drops 20%. You wait. It goes up 15%, and you still wait for “a bigger drop.” It goes up another 30%, and you finally invest—at a price higher than when it dropped.

Time in the market beats timing the market. Every single time. Invest consistently regardless of price, and you win.

Mistake #2: Panic Selling

You invest $500. Three months later, the market drops 12%. Your account drops from $500 to $440. Panic sets in, and you sell everything.

Then the market recovers 35% the next year, and you watch from the sidelines with your $440 in cash.

This is the most expensive emotion. Markets go down. That’s normal. You don’t sell at the bottom.

Mistake #3: Not Diversifying

Putting all your money in one company stock or one sector feels exciting when it goes up. It’s devastating when it doesn’t.

A single bad quarter at one company can tank your investment. A diversified portfolio spreads that risk across hundreds of companies. One company’s problems barely register.

Mistake #4: Ignoring Fees

You find a fund with a 1.2% expense ratio because it has a “cool” name. Over 40 years, that extra 1% compounds into hundreds of thousands of dollars you didn’t keep.

Always check the expense ratio. Use tools like Emergency Fund Calculator Target Amount to understand how much emergency savings you need before investing (this prevents panic selling when life happens).

Mistake #5: Checking Your Balance Too Often

Humans aren’t wired for investing. We evolved to notice short-term threats. Checking your balance daily triggers anxiety, and anxiety triggers bad decisions.

Check monthly. That’s enough.

Part 5: Building a Long-Term Investing Habit

Automatic Contributions: The Secret Weapon

Set up automatic monthly investments. $50, $100, $500—whatever you can afford. Have it automatically deducted from your checking account on payday.

Why this works: You never see the money, so you don’t miss it. You can’t talk yourself out of it. You’re dollar-cost averaging—buying more shares when prices are low, fewer when prices are high. This smooths out market volatility.

Set it and forget it. Literally. For 10, 20, 30 years if you can.

Quarterly Rebalancing

Every three months, take 30 minutes to:

- Check your asset allocation

- Rebalance if it’s drifted more than 5% from your target

- Review your expense ratios

- Note your new balance

This is maintenance, not obsession. It keeps you aligned without constant tinkering.

Regular Progress Reviews

Every six months, sit down and check your progress. Look at:

- Total contributions vs. total balance

- Returns vs. benchmarks

- Whether your plan is still aligned with your goals

Use a tracker like our Down Payment Savings Planner Home if you’re investing toward a specific goal, or our Net Worth Tracker and Dashboard Assets for overall wealth building.

Adjust Your Contributions Over Time

You started with $50/month. After a year, can you make it $100? After two years, $200?

Even small increases compound dramatically. An extra $50/month for 25 years is another $150,000+ in wealth.

Part 6: Your Investing Checklist

Here’s your action plan:

-

Open an account with a beginner-friendly brokerage (Fidelity, Vanguard, Charles Schwab, or Betterment)

-

Fund your first $50-100

-

Buy your first index funds (S&P 500 index fund + international index fund recommended)

-

Set up automatic monthly contributions

-

Create a simple tracking spreadsheet

-

Invest automatically every month

-

Review quarterly

-

Rebalance twice a year

-

Don’t panic when markets drop

-

Stay the course

If you’re juggling multiple financial goals, start here: use our 50-30-20 Budget Calculator Needs Wants to ensure you’re budgeting correctly, then our Emergency Fund Calculator Target Amount to build your safety net before investing.

Download Your Investment Starter Checklist

Ready to start but want a complete roadmap? Get our free Investment Starter Checklist — a step-by-step guide covering everything from choosing your first brokerage to setting up automatic contributions.

Conclusion: Start Now, Not Later

Investing isn’t complicated. It’s not exclusive. It’s not about having a lot of money right now—it’s about understanding compound growth and staying consistent over time.

$50 today becomes $79,000 over 30 years. But it only happens if you start.

You don’t need to be perfect. You don’t need to pick winning stocks. You don’t need to understand derivatives or hedge funds or any of the fancy stuff.

You need:

- A simple portfolio of low-cost index funds

- Automatic monthly contributions

- The discipline to not panic sell

- Patience

That’s it. That’s the whole system.

If you’re serious about building wealth, start this week. Open that account. Make your first investment. Set up automatic contributions. Then let compound interest do what it does best—turn small, consistent actions into substantial wealth over time.

Your future self will thank you for the decision you make today.

Ready to Manage Your Finances Better?

Explore our complete toolkit for financial success:

- Net Worth Tracker and Dashboard Assets — Track your complete financial picture

- Emergency Fund Calculator Target Amount — Know exactly how much you need saved

- 50-30-20 Budget Calculator Needs Wants — Master the proven budgeting method

- Down Payment Savings Planner Home — Plan for major financial goals

- Landlord Expense Tracker Rental Property — For those ready to invest in real estate

Start your investing journey today. Your future wealth starts with the decision you make right now.

Keep Reading

- I Tested 9 Expense Tracker Apps for 3 Months — Here’s What Actually Worked

- Freelancer Finance Management Dashboard (VVS): Finally, a Money Tool Built for Variable Income

- Airbnb Revenue Calculator: Estimate Your Short-Term Rental Income Before You List

Keep reading (related guides):

- Never Work Again Calculator: The Exact Number by Age

- How Much Money You Need to Retire Early at 40, 45, and 50 (Real Numbers by Age)

- How to Calculate Your Net Worth (And Why Its the Only Financial Number That Matters)

- Savings Rate Calculator: The One Number That Predicts Your Financial Future

- Bakery Revenue Calculator

Andy Gaber is the founder of Digital Dashboard Hub, a suite of 255+ interactive financial, productivity, and wellness tools. He built DDH after getting frustrated with financial apps that gave outputs without context. Follow along for tool tutorials, revenue analytics breakdowns, and honest takes on personal finance.