Buying your first home is one of life’s biggest milestones—and one of the most daunting. You’ve probably heard the conventional wisdom: “You need 20% down.” But here’s what most people don’t realize: that number is a myth. Understanding what you actually need, creating a realistic timeline, and choosing the right savings strategy can make homeownership feel achievable instead of impossibly distant.

About this article: I’m Andy, founder of Digital Dashboard Hub. I built DDH’s 255 free interactive tools to solve the specific financial, productivity, and wellness tracking gaps I kept seeing — starting with the problem this article covers. The free tool below is available without signup and works instantly. Try it and see your numbers in real time.

In this guide, we’ll break down exactly how much you need to save, where to park your money, and how to stay motivated through the entire process. Whether you’re dreaming of buying in 18 months or three years, a solid down payment savings plan is your first step toward the keys to your new home.

The Truth About Down Payment Requirements: Debunking the 20% Myth

Scroll down — the interactive tool runs live with your inputs. Full version lives inside Digital Dashboard Hub. Two-click trial, Stripe-secure.

Let’s start with the biggest misconception in home buying: you do NOT need 20% down to purchase a home.

The 20% rule became popular decades ago because it offered enough equity to avoid PMI (private mortgage insurance) and showed lenders you were financially responsible. But it’s not a requirement—it’s a preference that benefits banks, not buyers.

Here’s what you actually need for different loan types:

-

Minimum down payment: 3.5%

-

Best for: First-time buyers with lower credit scores or savings

-

Example: On a $250,000 home, you’d need just $8,750 down

-

Trade-off: You’ll pay mortgage insurance premiums, but they’re often lower than conventional PMI

-

Minimum down payment: 3-5% (some lenders offer 3% programs)

-

Best for: Buyers with good credit and stable income

-

Example: On a $250,000 home, you’d need $7,500-$12,500 down

-

Trade-off: PMI required until you reach 20% equity

-

Minimum down payment: 0%

-

Best for: Military members, veterans, and eligible spouses

-

Example: Purchase a $250,000 home with zero down

-

Trade-off: Limited to eligible applicants, but no PMI

-

Minimum down payment: 0%

-

Best for: Rural property purchases; income limits apply

-

Example: Zero down for qualifying rural properties

-

Trade-off: Geographic restrictions; must meet income requirements

The takeaway? Most first-time buyers can purchase a home with 3-5% down. That dramatically changes what you need to save.

How Much Down Payment Do You Actually Need to Save?

The amount you need depends on your target home price and loan type. Let’s work through realistic scenarios:

-

Down payment: $10,000

-

Closing costs (3%): $6,000

-

Total upfront: $16,000

-

Emergency cushion: $2,000

-

Total to save: $18,000

-

Down payment: $10,500

-

Closing costs (3%): $9,000

-

Total upfront: $19,500

-

Emergency cushion: $3,000

-

Total to save: $22,500

-

Down payment: $17,500

-

Closing costs (4%): $14,000

-

Total upfront: $31,500

-

Emergency cushion: $5,000

-

Total to save: $36,500

Notice something? Closing costs matter as much as the down payment itself. Many first-time buyers focus only on the down payment and get blindsided by closing costs at the end. We’ll cover this more in detail later, but the key is: plan for both.

Creating Your Down Payment Timeline: When Do You Want to Buy?

| Option | Cost | Time Investment | Customizable? | Best For |

|---|---|---|---|---|

| DIY approach | Free | High | Fully | Those with time to build from scratch |

| Generic tool | $5-$50/mo | Medium | Limited | Standard use cases |

| DDH Free Tool | Free trial | 5-10 min setup | Yes | Getting real answers without spreadsheet hell |

The timeline you choose determines how aggressive your savings plan needs to be. Here are realistic savings targets based on different timeframes:

-

Monthly savings needed: $834

-

Strategy: Cut expenses, redirect bonuses/tax refunds, negotiate raises

-

Best for: Buyers who can’t wait and have stable income

-

Save with our Down Payment Savings Planner to track progress

-

Monthly savings needed: $833

-

Strategy: Automate savings, invest in high-yield accounts, side income

-

Best for: Most first-time buyers; allows breathing room

-

Use this timeline to explore first-time buyer programs you might qualify for

-

Monthly savings needed: $833

-

Strategy: Aggressive saving with more flexibility, explore wealth-building strategies

-

Best for: Building substantial equity, avoiding PMI entirely

-

More time to improve credit and financial profile

The three-year timeline is sweet spot for most buyers. It’s aggressive enough to feel like real progress, yet realistic enough to maintain without derailing your entire budget.

Where to Park Your Down Payment Savings

This is crucial: do not invest your down payment in the stock market. Your down payment has a specific deadline. Market volatility could sabotage your timeline.

Instead, use these low-risk, accessible options:

-

Current rates: 4.5-5.0% APY (as of 2024-2025)

-

Liquidity: Instant access (within 1-2 days)

-

Pros: FDIC insured, no risk, attractive returns

-

Cons: Rates fluctuate

-

Best for: Your primary down payment fund

-

Start tracking with Savings Goal Tracker

-

Current rates: 4.5-5.3% APY for 1-2 year terms

-

Liquidity: Locked in until maturity (penalty for early withdrawal)

-

Pros: FDIC insured, higher rates than HYSA, predictable

-

Cons: Limited access

-

Best for: Funds you won’t need for 12-24 months

-

Current rates: 4.5-5.0% APY

-

Liquidity: Generally accessible with check-writing capability

-

Pros: FDIC insured, better rates than savings

-

Cons: May have minimum balances or withdrawal limits

-

Best for: Flexible access combined with higher yields

-

Put your primary down payment fund in a HYSA for accessibility

-

Use a 12-month CD for funds you won’t touch

-

Keep closing cost estimates in a separate HYSA

-

Build a separate emergency fund (don’t raid your down payment fund for surprises)

First-Time Buyer Programs That Actually Help

You likely qualify for programs you’ve never heard of. These can dramatically reduce your required down payment:

-

Lower down payments (3.5%)

-

More lenient credit requirements

-

Income limits: None

-

Drawback: Mortgage insurance costs

-

Many states offer grants or forgivable loans for down payments

-

Examples: California’s CalHFA, New York’s Homes and Community Renewal

-

Typical assistance: $5,000-$15,000

-

Application: Through participating lenders

-

Check your state’s housing authority website

-

Tech companies, major corporations offer down payment help

-

Typical assistance: $5,000-$25,000

-

Best for: High-earning employees

-

Ask your HR department if this benefit exists

-

VA loans: Zero down for eligible veterans

-

USDA loans: Zero down for rural properties (income limits apply)

-

Saves: Entire down payment amount

These programs can slash your savings target from $30,000 to $15,000 or less. Worth investigating before you start saving aggressively.

The Closing Costs You Didn’t Budget For

Here’s where many first-time buyers get hurt: closing costs. These are fees charged when you finalize your mortgage. People focus so hard on the down payment that they forget about this critical expense.

On a $300,000 home:

-

2% closing costs: $6,000

-

5% closing costs: $15,000

-

Loan origination fees (0.5-1%)

-

Appraisal fee ($300-$500)

-

Title search and insurance ($500-$1,500)

-

Property inspection ($300-$500)

-

Survey ($200-$500)

-

Attorney/escrow fees ($500-$1,500)

-

Recording fees ($100-$300)

-

Credit report fees ($15-$50)

-

Home warranty ($300-$500)

-

Taxes and insurance prorations (varies)

Pro Tip: Use our Home Affordability Calculator to estimate true costs based on your target purchase price. Then add 10% as a safety buffer.

Automate Your Savings and Stay Motivated

The difference between people who save $30,000 and those who save $5,000? Automation.

-

Schedule weekly or biweekly transfers to your HYSA the day after payday

-

Removes temptation and willpower from the equation

-

Even $200/paycheck = $5,200/year

-

Use our Monthly Budget Planner to identify where to redirect funds

-

Use a Savings Goal Tracker to watch your progress

-

Calculate your monthly milestone

-

Celebrate when you hit 25%, 50%, 75%, and 100%

-

Pin pictures of homes you love to Pinterest

-

Drive through neighborhoods you want to live in

-

Imagine your life in your new space

-

When motivation fades, remember why you started

-

Emergency expenses happen (car repairs, medical bills)

-

Don’t abandon your goal if you have one setback month

-

Build a separate emergency fund so you don’t raid your down payment savings

-

See our Emergency Fund Tracker to keep these separate

Understanding PMI: When You Need It, What It Costs, and Whether to Avoid It

Private Mortgage Insurance (PMI) is a hot topic among first-time buyers. Here’s what you actually need to know:

-

You put down less than 20%

-

Required on conventional loans

-

Not required on FHA, VA, or USDA loans (they have different insurance)

-

Typically 0.5-2% of your loan amount annually

-

On a $250,000 loan with 5% down ($12,500), PMI might be $100-$400/month

-

You can remove PMI once you reach 20% equity (roughly when home appreciates + you pay down principal)

This depends on your situation:

-

You can save 20% down in a reasonable timeline (3-4 years)

-

Your rate won’t improve significantly with a larger down payment

-

You’d be extremely house-poor trying to reach 20%

-

You’re tired of renting and missing out on home equity growth

-

You can pay down to 20% equity within 5-7 years

-

Waiting another 2-3 years means paying more rent

-

Interest rates might rise

The Math: If you can save $50,000 for 20% down on a $250,000 home, or $15,000 for 5% down today, buying now and paying PMI might actually cost less than renting while you save. Run the numbers.

Your Action Plan: Start Today

You now have everything you need to create a down payment savings plan:

- Identify your target home price and calculate your required down payment + closing costs

- Choose your timeline (18 months, 3 years, or 5 years)

- Determine your monthly savings goal

- Research first-time buyer programs in your area

- Open a high-yield savings account and set up automatic transfers

- Track your progress with a savings goal tracker

- Get pre-approved to understand your actual borrowing power

Ready to Take Control of Your Down Payment Savings?

Creating a down payment plan doesn’t require a financial advisor or expensive tools—but it does require clarity and discipline. We built the Down Payment Savings Planner specifically for first-time buyers like you, with built-in calculators for timelines, closing costs, and PMI impact.

Download our free Down Payment Savings Roadmap to get a customizable timeline, expense tracker, and monthly savings guide tailored to your target purchase price and timeline.

Your first home is closer than you think. With the right plan and the right tools, you’ll be holding those keys sooner than you expect.

Keep reading (related guides):

- Business Expense Tracker: Categorize and Export for Tax Time

- How Much Money You Need to Retire Early at 40, 45, and 50 (Real Numbers by Age)

- ADHD Impulse Spending Tracker: See Where Your Money Disappears (Free Tool)

- Holiday Budget Planner: How to Survive December Without Going Into Debt

- Auto Mechanic Revenue: What Owners Make vs. What Youd Expect (2026)

255+ interactive tools for your money, time, and health.

14 days free · No charge today · 2-click cancel

Keep Reading

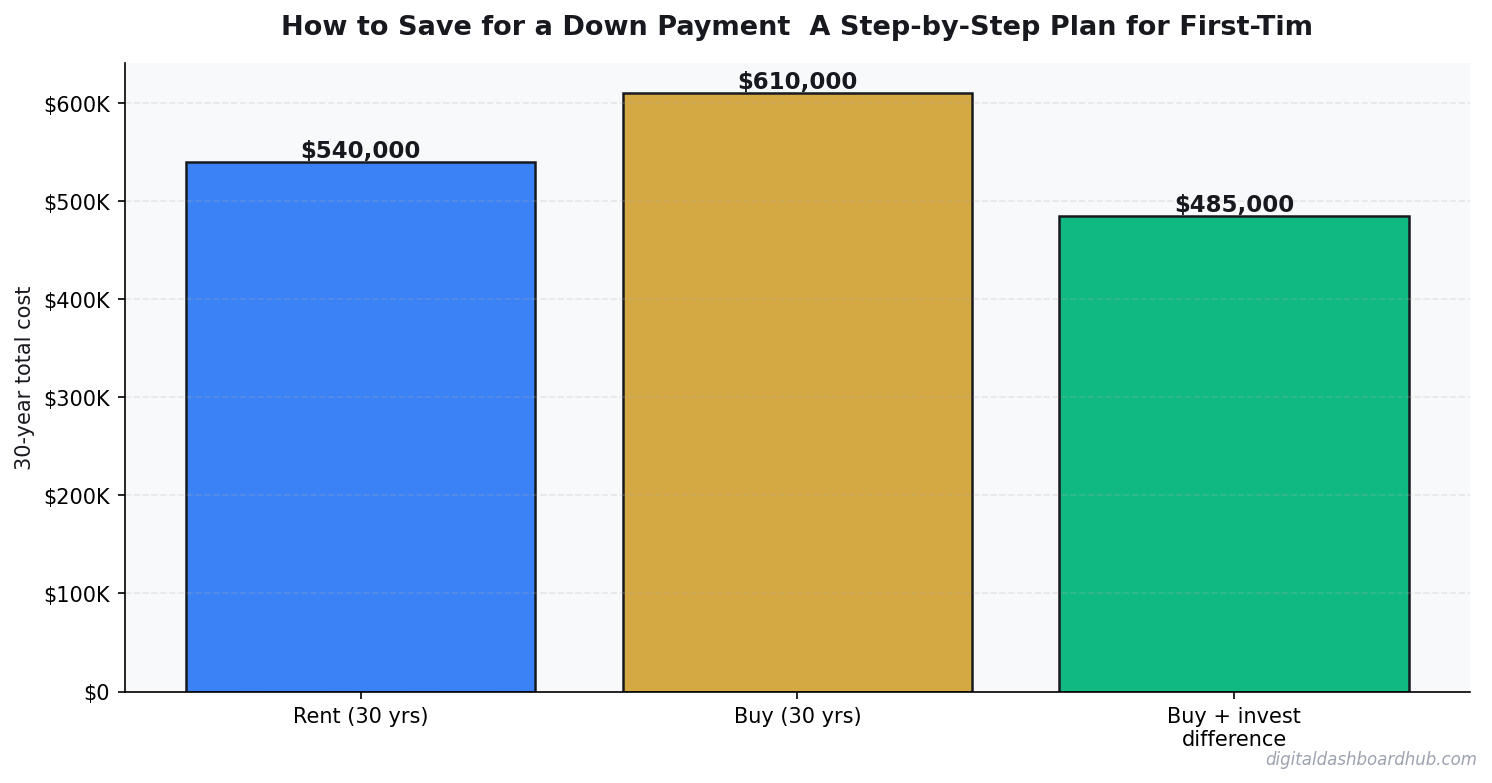

- Rent vs. Buy Calculator 2026: The True Cost of Each Option (Real Numbers)

- Compound Interest Calculator: Why Starting Now Beats Starting Smart Later

- You’re Probably Wasting $200/Month on Subscriptions You Forgot About (Here’s How to Find Them)

Andy Gaber is the founder of Digital Dashboard Hub, a suite of 255+ interactive financial, productivity, and wellness tools. He built DDH after getting frustrated with financial apps that gave outputs without context. Follow along for tool tutorials, revenue analytics breakdowns, and honest takes on personal finance.