Introduction

Before you scroll: the calculator below is running in your browser right now. For the full feature set — saved scenarios, history, exports — open the dashboard.

Remember when your grandmother kept cash in separate envelopes labeled “Rent,” “Groceries,” and “Entertainment”? There’s a reason that system worked for generations. But in 2026, physically stuffing envelopes with cash feels outdated—until you realize that the psychology behind it is timeless.

The envelope budgeting system has made a major comeback, but with a modern twist. Thousands of people are ditching complicated budgeting apps and embracing a digital cash envelope system using spreadsheets, which combines the psychological power of the original method with the convenience of digital tracking.

here, we’ll explore everything you need to know about cash envelope budgeting, whether you’re considering going digital, keeping it physical, or blending both approaches.

What Is the Cash Envelope System and Why Does It Actually Work?

The envelope budgeting system is refreshingly simple: you allocate money to specific spending categories by putting physical cash (or in the digital version, tracked funds) into designated “envelopes.” When the envelope is empty, you’re done spending in that category until the next budgeting period.

The Psychology Behind the Envelope System

This method works because it leverages three powerful psychological principles:

When you physically hand over cash or watch your digital envelope total decrease, you feel the impact immediately. This is called the “pain of payment.” You’re not swiping a card that feels frictionless—you’re watching real money leave. This creates natural spending discipline without willpower.

Seeing an envelope labeled “Entertainment: $75” makes spending limits concrete and memorable. Your brain processes visual information faster than numbers on a bank statement. You instantly know where you stand in each category.

With limited envelopes and limited cash, you must decide what matters most. Should that $30 go to dining out or streaming subscriptions? This decision-making strengthens your financial awareness and aligns spending with values.

Research in behavioral economics supports this. Studies show that people spend significantly less when using cash compared to credit or debit cards, and structured allocation methods (like envelopes) create even better results.

Digital Envelope Budgeting vs. Physical Cash Envelopes: Pros and Cons

| Method | Time to Set Up | Accuracy | Automation | Best For |

|---|---|---|---|---|

| Spreadsheet (manual) | 2-4 hours | High (if maintained) | None | Detail-oriented budgeters |

| Budget apps (Mint/YNAB) | 30-60 min | Medium (syncing errors) | Bank sync | Hands-off tracking |

| DDH Financial Dashboard | 5-10 min | High (you control inputs) | Interactive calculator | Freelancers, variable income, small business owners |

Both approaches work—the best choice depends on your lifestyle and preferences.

Physical Cash Envelopes

-

Maximum psychological impact—nothing beats the feeling of cash

-

Complete privacy (no digital trace)

-

No technology required; works during outages

-

Perfect for overspenders who need extreme accountability

-

Tactile satisfaction of the system

-

Less secure (loss, theft, damage)

-

Harder to track historical spending patterns

-

Inconvenient for online purchases

-

Manual counting and reconciliation required

-

Difficult to handle variable expenses (medical bills, car repairs)

Digital Cash Envelope System (Spreadsheets)

-

Works for online and in-person spending

-

Automatic calculations and tracking

-

Easy to review spending history and trends

-

Adjustable for variable income and expenses

-

Secure cloud backup options

-

Real-time updates from multiple devices

-

Less tactile—easier to ignore spending limits

-

Requires digital discipline (not just cash discipline)

-

Temptation to edit the spreadsheet when you overspend

-

Setup requires some technical comfort

The Hybrid Approach: Many successful budgeters use both. They might keep physical envelopes for discretionary spending (dining, entertainment) to maintain the psychological edge, while using digital tracking for bills and subscriptions.

The digital envelope system has gained traction because it solves the biggest problem with physical envelopes: online shopping. If you spend 40% of your budget online, stuffing physical envelopes becomes impractical.

How to Set Up Your Digital Envelope Categories

Setting up your digital cash envelope system correctly is crucial. Here’s the process:

Step 1: Identify Your Spending Categories

Start with these common categories, then customize based on your life:

-

Rent or Mortgage

-

Utilities

-

Insurance

-

Debt Payments

-

Groceries

-

Transportation/Gas

-

Medical/Healthcare

-

Household Maintenance

-

Childcare (if applicable)

-

Dining Out/Coffee

-

Entertainment

-

Hobbies

-

Personal Care

-

Shopping (clothing, home goods)

-

Emergency Fund

-

Retirement

-

Vacation Fund

-

Vehicle Replacement Fund

Don’t create too many categories (analysis paralysis) or too few (they become useless). Most successful budgeters use 8-15 categories.

Step 2: Calculate Monthly Allocations

Use your past 3 months of spending to determine realistic amounts. If you’ve spent an average of $280 on groceries monthly, that’s your starting point. Don’t underestimate categories or you’ll abandon the system.

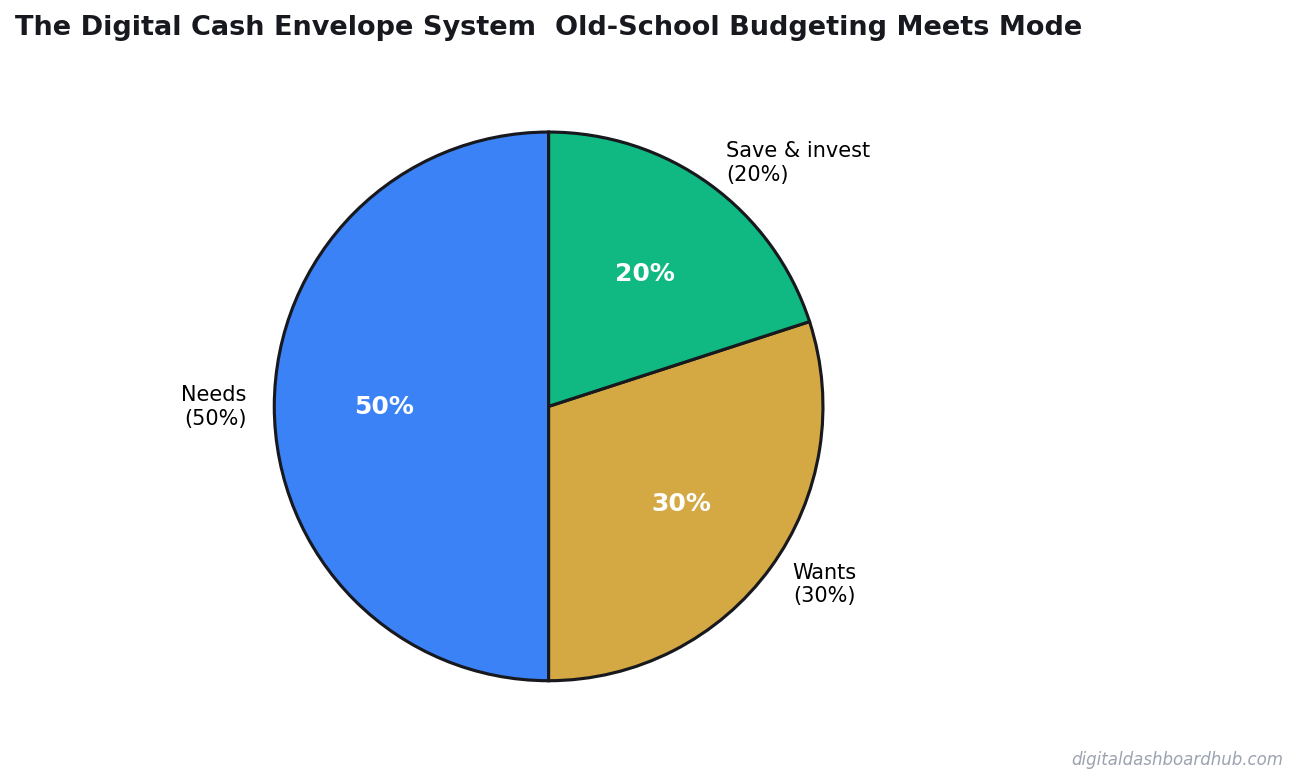

If your income varies, use the 50/30/20 rule as a starting framework: 50% for needs, 30% for wants, 20% for savings. Our 50/30/20 Budget Calculator can help you quickly allocate your income using this proven method.

Step 3: Set Up Your Spreadsheet

Your spreadsheet should include:

- Category name

- Allocated amount

- Spent amount (updated as you purchase)

- Remaining balance (automatic calculation)

- Notes column (optional, for tracking large purchases)

Color-coding helps: green for healthy envelopes, yellow for low balance, red for over budget.

Step 4: Choose Your Tracking Method

Will you:

- Log purchases immediately after buying?

- Batch them daily or weekly?

- Use bank transaction imports to auto-fill (if your spreadsheet allows)?

The best method is whatever you’ll actually do consistently. Daily logging provides maximum awareness; weekly works well if you prefer less frequent updates.

For a complete, ready-to-use digital envelope system, our Cash Envelope Budget Google Sheets template handles all calculations automatically and includes pre-built categories you can customize.

Common Mistakes People Make With Envelope Budgeting

Even with the best intentions, people sabotage their own envelope systems. Watch out for these pitfalls:

Mistake #1: Unrealistic Category Amounts

This is the #1 reason people abandon the system. They drastically cut spending amounts to “encourage discipline,” then feel deprived and quit.

approach: Start with amounts that match your actual spending. Once the system becomes automatic, you can gradually reduce categories if needed.

Mistake #2: Forgetting to Update Your Spreadsheet

Digital envelopes only work if you track spending. Letting receipts pile up means your spreadsheet becomes useless fiction.

approach: Set a specific time (daily or weekly) for updates. Make it a 5-minute ritual you don’t skip. Set a phone reminder if needed.

Mistake #3: Creating Bloated “Miscellaneous” Categories

One catch-all category defeats the purpose. You lose the targeting benefit of specific allocations.

approach: Break down “Miscellaneous” into actual categories. Can’t justify the size? It probably doesn’t deserve a separate envelope.

Mistake #4: Ignoring Variable Expenses

Many people start with categories only for regular monthly expenses, then panic when irregular bills arrive.

approach: Create “sinking fund” envelopes for irregular expenses: car maintenance, annual subscriptions, home repairs. Divide the annual cost by 12 and set aside that amount monthly.

Mistake #5: Staying Too Rigid

Life happens. Your dog needs a $300 vet visit. Rigidly refusing to use the entertainment envelope for this legitimate expense causes frustration.

approach: Build small “emergency buffer” into your system (5-10% of total budget). Allow flexibility when genuine needs arise, then recalibrate next month.

Mistake #6: Not Reviewing Your System

Setting up envelopes and ignoring them for six months wastes the entire point. You won’t learn anything about your spending patterns.

approach: Review your envelopes monthly. Identify patterns. Did entertainment consistently exceed $150? Adjust. Did groceries come in under budget? Celebrate that win and consider redirecting savings.

Making the Envelope System Work Long-Term

Start Small: Don’t try to track every expense immediately. Many successful users start with just 5-6 key categories, then expand once the habit sticks.

Use Tools Designed for This: Generic spreadsheets work, but templates specifically built for envelope budgeting handle the calculations and updates more efficiently. A well-designed Monthly Budget Planner includes envelope tracking plus monthly and yearly insights.

If You’re Paid Biweekly: Standard monthly envelopes might not align with your paychecks. A Biweekly Budget Template resets your envelopes every two weeks, matching your cash flow to your spending periods.

Track More Than Just Spending: Understanding where every paycheck dollar goes is powerful. Our Paycheck Breakdown Analyzer shows you exactly how much goes to taxes, benefits, and take-home pay—essential for accurate envelope budgeting.

Build an Emergency Fund Envelope: Most people do envelope budgeting because they want to control spending and build savings. Don’t neglect this. Our Emergency Fund Calculator determines exactly how much you need and creates a roadmap to get there.

Digital Cash Envelope Budgeting for Different Life Situations

Couples: One spreadsheet, shared editing access, color-coded rows for his/her spending, or separate envelopes per person. Communication is critical.

Single Income, Multiple Dependents: Use larger allocations for groceries and childcare. Consider a separate entertainment envelope for kids’ activities.

Freelancers/Variable Income: Base your envelopes on your average monthly income, not best-case scenarios. Build extra-large savings envelopes to smooth out feast-and-famine months.

Debt Payoff Focus: Create specific envelopes for each debt, or one aggressive “debt payment” envelope. This method pairs perfectly with debt-focused goals.

Conclusion

The digital cash envelope system combines the best of old-school budgeting psychology with modern convenience. Whether you choose purely digital, purely physical, or a hybrid approach, the key is choosing a method you’ll stick with.

The envelope system isn’t about restriction—it’s about intentionality. It’s about knowing exactly where your money goes and ensuring that money supports your actual priorities, not just your impulses.

Start this week. Choose five categories. Allocate amounts based on real spending, not fantasy numbers. Then commit to 30 days of consistent tracking. You’ll be shocked by what you learn about your spending patterns, and you’ll develop genuine control over your finances.

Ready to Master Your Budget?

The envelope system works even better when you have the right tools. Download our free Digital Envelope Category Planner—a customizable guide that walks you through identifying categories, calculating allocations, and setting up your tracking system in under an hour.

[Sign up with your email to receive the planner instantly]

Looking for a complete approach? Our Cash Envelope Budget Google Sheets template does all the calculations for you, with color-coded tracking and automatic balance updates. Start budgeting like you mean it today.

Published: March 2026 | Reading Time: 8 minutes | Author: Digital Dashboard Hub

Keep Reading

- I Tested 9 Expense Tracker Apps for 3 Months — Here’s What Actually Worked

- Freelancer Finance Management Dashboard (VVS): Finally, a Money Tool Built for Variable Income

- Airbnb Revenue Calculator: Estimate Your Short-Term Rental Income Before You List

Keep reading (related guides):

- Business Expense Tracker: Categorize and Export for Tax Time

- How Much Money You Need to Retire Early at 40, 45, and 50 (Real Numbers by Age)

- Restaurant Revenue vs. Expenses: Why $1M in Sales Can Mean $50K in Profit

- Sinking Fund Savings Goal Planner: The Free Visual Dashboard That Kills Surprise Expenses

- A/B Testing Your Etsy Listings: How to Know Whats Actually Working

255+ interactive tools for your money, time, and health.

Full dashboard access · Stripe-secure checkout · Cancel anytime

Andy Gaber is the founder of Digital Dashboard Hub, a suite of 255+ interactive financial, productivity, and wellness tools. He built DDH after getting frustrated with financial apps that gave outputs without context. Follow along for tool tutorials, revenue analytics breakdowns, and honest takes on personal finance.